I used to think travel money was simple: grab some cash, swipe a card, done. Then I started adding up the numbers. Between bad exchange rates, ATM fees, and sneaky convenience

charges, I realised my payment choices were quietly adding 10–20% to every trip.

If you’re spending $2,000–$3,000 on a holiday, that’s $200–$600 gone… just because of how you paid.

In this guide, I’ll walk you through the real trade-offs between cash, cards, and payment apps abroad – and how to build a simple system that keeps those hidden costs as close to 0% as possible.

1. The Silent Budget Killer: How Payment Choices Add 10–20% to Your Trip

Here’s the uncomfortable bit: you can plan the perfect itinerary, find great flight deals, book smart accommodation… and still overpay badly just by choosing the wrong way to pay.

Most of that extra 10–20% comes from a handful of quiet culprits:

- Bad exchange rates at airport kiosks and some banks (often 4–12% worse than the real market rate).

- Foreign transaction fees on many cards (typically 3–7% per purchase).

- ATM fees from both your bank and the foreign bank.

- Dynamic Currency Conversion (DCC) – that friendly

Pay in your home currency?

prompt that usually hides a 3–7% markup. - Cash-only traps where you’re forced into bad last-minute exchanges because you didn’t plan ahead.

Put those together and it’s easy to lose 10–15% of your budget without noticing. As BestExchangeRates and GoTripper both point out, disorganised travel money is one of the fastest ways to burn cash on a trip.

My rule of thumb: if you don’t think about how you’ll pay abroad, assume you’re tipping the financial system an extra 10–20% for the privilege of travelling.

2. Cash Abroad: When It Saves You Money (and When It Bleeds You Dry)

Cash feels straightforward. Hand it over, get your food, your ticket, your room key. No machines, no apps, no fuss.

But when you look at the real cost of cash vs card abroad, cash is often where travellers lose the most.

When cash is your friend:

- In cash-heavy cultures – think Japan, Germany, rural Southeast Asia, parts of Africa and Latin America.

- For small purchases: street food, markets, tips, local buses, small guesthouses.

- When you’re in areas with unreliable card terminals or frequent power cuts.

- In countries with dual or informal rates (e.g. Argentina, Turkey, Egypt, Lebanon), where understanding the real market rate can almost double your spending power.

When cash quietly drains your budget:

- You buy it at the airport or hotel desk (often 5–12% worse than a bank ATM).

- You exchange too much and end up converting back at another bad rate.

- You withdraw small amounts frequently, paying fixed ATM fees every time.

- You carry so much that theft or loss becomes a serious financial hit.

Most modern travel money guides – from CityGenie to Alpha-Keeper – land on the same idea: cash is essential, but it should be the minority of your spending.

Practical cash strategy I use:

- Arrive with $100–$200 equivalent in local currency for the first 24 hours.

- Withdraw more from bank ATMs in town, not airport kiosks or hotel machines.

- Keep total cash on you under ~$300 in most developed destinations.

- Split cash between your wallet, day bag, and a hidden spot (money belt / hotel safe).

The goal isn’t to avoid cash. It’s to avoid buying cash badly and getting stung by hidden travel payment fees.

3. Cards: Your Best Tool – or a 7% Tax on Every Purchase?

Used well, cards are usually the cheapest way to pay abroad. Used badly, they turn into a quiet 3–7% tax on everything you buy.

Here’s how I think about the cash vs card travel cost comparison.

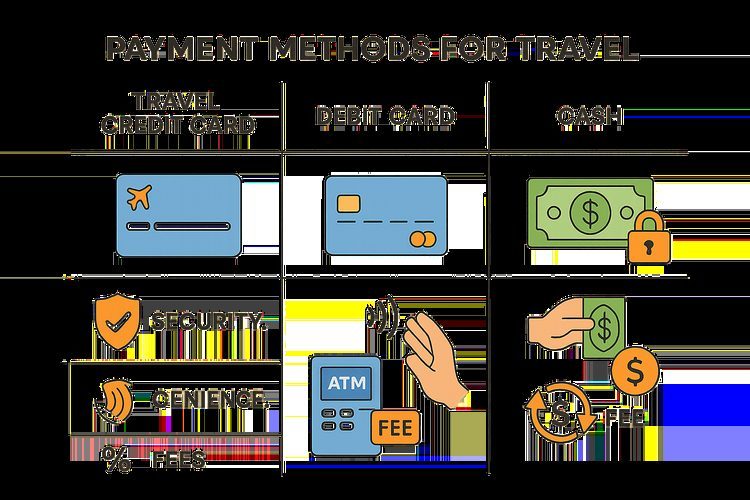

Credit cards – my default for most purchases

- Pros: strong fraud protection, rewards, easy to dispute charges, often better exchange rates than cash exchanges.

- Cons: many still charge 3% foreign transaction fees; interest if you don’t pay in full; some add hidden FX markups.

What I look for in a travel credit card:

- No foreign transaction fees (this alone can save 3–7% vs traditional bank cards).

- Visa or Mastercard for the widest global acceptance.

- Chip-and-PIN + contactless for Europe, transit systems, and tap-to-pay countries.

Debit cards – my tool for getting cash, not for everyday spending

- Pros: cheap way to withdraw local currency from ATMs, especially with banks that refund ATM fees or belong to global alliances.

- Cons: weaker fraud protection; stolen funds come straight from your account; you can get hit with international ATM withdrawal fees from both banks.

What I look for in a debit card:

- A bank that refunds international ATM fees or charges very little.

- No or low FX margin on withdrawals (watch for hidden exchange rate markup on trips).

The big card traps that cost you real money:

- Foreign transaction fees: 3% on every purchase adds up fast over a full trip.

- Dynamic Currency Conversion (DCC): when a terminal asks

Pay in USD/EUR/GBP?

– this almost always uses a terrible rate. Always choose local currency. - Cash advances on credit cards: high fees + interest from day one. I avoid this completely.

My card setup:

- 1 main no-foreign-fee credit card (Visa or Mastercard).

- 1 backup credit card from a different network (e.g. if the main is Visa, backup is Mastercard).

- 1 debit card with low ATM fees for cash withdrawals.

- Store them in different places so one theft doesn’t wipe you out.

Used this way, cards are usually the best payment method for overseas travel – cheap, flexible, and easier to secure if something goes wrong.

4. Payment Apps & Digital Wallets: Convenience vs. Connectivity Risk

Apple Pay, Google Pay, Wise, Revolut, local QR apps… it’s tempting to think you can travel with just your phone now.

In some places, that’s almost true. In others, it’s a fast way to get stuck at a checkout with no way to pay.

Where apps and wallets shine:

- In highly digital countries like Sweden, the UK, the Netherlands, Australia, and much of North America.

- In places that leapfrogged to QR/app payments – parts of China (Alipay/WeChat), India (UPI), and some Southeast Asian cities.

- For budgeting: prepaid or multi-currency apps (Wise, Revolut, etc.) let you load a fixed amount and track spending in real time.

- For better FX rates than many traditional banks, especially on multi-currency cards.

Where they can backfire:

- You lose your phone or it dies. No battery = no money.

- You don’t have reliable data or can’t receive SMS codes to approve payments.

- Local systems don’t accept your app (e.g. Alipay without a Chinese account, or local QR apps that require a local ID).

- Hotels and car rentals block large deposits on prepaid cards, tying up your travel funds.

As VoyeGlobal and others point out, digital wallets are only as good as your connectivity. No data, no app, no money.

How I use apps without depending on them:

- Use a multi-currency app card (Wise, Revolut, etc.) for day-to-day spending and ATM withdrawals where it’s cheap.

- Keep a traditional credit card for hotels, car rentals, and emergencies.

- Download apps for local payment systems only if they’re widely used and easy for foreigners to join.

- Make sure I have a reliable data plan or eSIM so my banking apps actually work abroad.

The cost of using payment apps abroad can be low, but I still treat them as part of a hybrid system, not a single point of failure.

5. Country Reality Check: Cash-Heavy vs. Card-First vs. App-Obsessed

One of the biggest travel payment mistakes I see is assuming your home habits apply everywhere. They don’t.

Some countries are almost cashless. Others still run on banknotes. Some jump straight to QR codes and local apps.

Mostly card-first (you can go light on cash):

- Nordic countries (Sweden, Norway, Denmark) – many places are effectively cashless.

- UK, Netherlands, Australia, much of North America – tap-to-pay is everywhere.

- Dubai, Singapore – very card and app friendly.

Cash-heavy or mixed (you need real cash):

- Japan & Germany – still surprisingly cash-reliant, especially small shops and inns.

- Rural Southeast Asia, parts of Africa, small towns worldwide – cash is king.

- Turkey, Spain, Thailand – cards in cities, but markets and small eateries often prefer cash; Thailand’s ATMs have high fixed fees, so withdraw larger amounts less often.

App/QR-heavy ecosystems:

- China – Alipay and WeChat Pay dominate.

- India – UPI and QR codes everywhere.

- Various cities in Southeast Asia – local QR apps and wallets are growing fast.

On top of that, some countries (Argentina, Turkey, Egypt, Lebanon) have unstable currencies and multiple exchange rates. In those places, how and where you exchange money can change your effective budget by 30–100%.

What I do before any trip:

- Search:

Country name cash or card Reddit

and read posts from the last 3–6 months. - Check if there are dual exchange rates or common unofficial rates.

- Look up whether my card network (Visa/Mastercard) is widely accepted.

The aim is simple: land already knowing whether this is a 70% card / 30% cash

destination or closer to 50/50

. That’s how you avoid nasty surprises and hidden travel payment fees.

6. The 70/30 Rule: A Simple Hybrid Strategy That Actually Works

Let’s turn all this into something you can actually use on your next trip.

For most developed destinations, I aim for roughly:

- 70% of spending on cards (credit + app-based cards).

- 30% in cash for small, cash-only, or rural situations.

For cash-heavy regions (Japan, Germany, rural Southeast Asia, parts of Africa), I shift closer to 50/50.

My default setup for a 1–2 week trip:

- Before I go

- Pick my main no-foreign-fee credit card and a backup.

- Choose a debit or app card with low ATM fees.

- Order a small amount of local cash if the destination is known to be cash-heavy.

- Notify my bank (or at least double-check travel settings in the app).

- On arrival

- Use my starter cash for transport, snacks, first meal.

- Find a bank ATM in town (not at the airport) and withdraw a sensible amount.

- During the trip

- Use credit card for hotels, restaurants, tickets, and larger purchases.

- Use debit/app card for ATM withdrawals and some everyday spending.

- Use cash for markets, tips, small shops, and anywhere that looks like card fees will be passed on.

- Always pay in local currency and decline DCC at terminals and ATMs.

Red flags I watch for at payment time:

- The terminal shows my home currency by default – I ask them to switch to local.

- The ATM offers a

guaranteed rate

orconversion

– I decline and choose without conversion if possible. - A merchant says

We can charge you in your home currency, it’s easier

– I politely refuse.

This hybrid approach is boring, which is exactly why it works. It spreads risk, keeps fees low, and helps you avoid the classic cash vs card vs payment apps travel mistakes that quietly inflate your trip cost.

7. Avoiding Disaster: Backup Plans, Connectivity & Security

Now for the part nobody likes to think about: what happens when something goes wrong?

Because on a long enough timeline, it will. A card gets blocked. An ATM eats your debit card. Your phone dies at the worst possible moment.

Card & cash backups I always have:

- At least two physical cards from different networks (e.g. Visa + Mastercard).

- One card stored separately from my wallet (hotel safe, hidden pocket, luggage).

- Emergency cash (the equivalent of $100–$200) hidden away for worst-case scenarios.

Connectivity safeguards:

- A reliable data plan or eSIM so I can access banking apps, OTP codes, and digital wallets.

- Offline copies of card numbers and bank contact info stored securely (e.g. password manager).

Security habits that actually matter:

- Use your bank/app to freeze a card instantly if it’s lost or skimmed.

- Don’t keep all cards and cash in one place – assume one bag could disappear.

- Be extra cautious at ATMs: cover the keypad, avoid sketchy standalone machines, and prefer those attached to real banks.

Think of it this way: your goal isn’t just to save 10–20%. It’s to make sure one lost card, one bad ATM, or one dead phone doesn’t end your trip.

8. Putting It All Together: Your Personal Money Mix

By now, the pattern is pretty clear:

- Cash is your local lubricant – essential, but expensive if you get it wrong.

- Cards are your workhorse – usually the cheapest way to pay abroad when you pick the right ones and dodge DCC.

- Apps & wallets are your accelerators – powerful, but only with good connectivity and a solid backup.

If you want a simple starting point for your next trip, here’s the checklist I’d actually print:

- ✔ One no-foreign-fee credit card (main).

- ✔ One backup credit card from a different network.

- ✔ One debit or app-based card with low ATM fees.

- ✔ $100–$200 equivalent in local cash for day one.

- ✔ A plan for where you’ll withdraw cash (bank ATMs, not airport kiosks).

- ✔ A data plan/eSIM so your banking apps and wallets actually work.

- ✔ A decision: is this destination 70/30 card-to-cash or closer to 50/50?

Once you’ve answered that last question for your specific destination, you’re no longer guessing. You’re running a deliberate money strategy – and that’s usually the difference between a trip that quietly leaks 15% and one where your money actually goes where you want it to: into experiences, not fees.