I’ve lost more money to bad exchange rates than to pickpockets. Not in dramatic ways. More like a slow leak of small

fees on flights, hotel bills, and ATM withdrawals that seemed harmless in the moment.

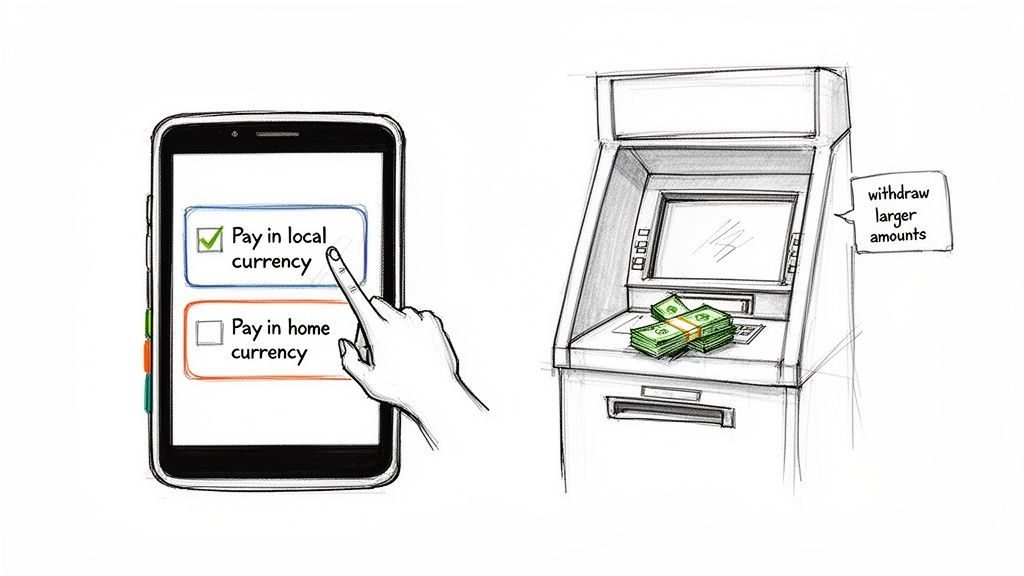

If you’ve ever stood at a card terminal abroad, staring at two options – pay in local currency or pay in your home currency – and just guessed, this guide is for you.

We’ll walk through the real choices you face on the road: cash vs card vs apps, airport kiosks vs ATMs, and that sneaky thing called Dynamic Currency Conversion (DCC). The aim is simple: help you avoid hidden currency conversion fees and stop overpaying just to spend your own money.

1. The Big Question at Checkout: Local Currency or Home Currency?

This is where many travelers quietly lose 5–9% without realizing it.

You hand over your card in Paris, Bangkok, or Mexico City. The terminal flashes two options:

- Pay in EUR / THB / MXN (local currency)

- Pay in USD / CAD / GBP (your home currency)

Paying in your home currency feels safer. You see a number you recognize. The screen might promise a guaranteed rate

or say cardholder’s currency

. It looks like a favor.

It usually isn’t. That’s Dynamic Currency Conversion (DCC).

Here’s what’s really going on behind that friendly-looking button:

- The merchant’s bank (or ATM operator) sets the exchange rate, not your card network.

- They add a hidden markup – often around 5–8%, sometimes more.

- You pay that markup on top of any credit card foreign transaction fees your bank charges.

When you choose local currency, your card network (Visa, Mastercard, etc.) usually converts at a wholesale rate that’s much closer to the real market rate. If your card has no foreign transaction fees, this is often the cheapest way to pay overseas.

My rule at checkout: when in doubt, always choose the local currency. If the screen is confusing, I pick the option that matches the country I’m in, not the country I’m from.

Quick mental script you can reuse:

- If the waiter asks,

Home currency or local?

I say:Local, please.

- If the terminal shows

cardholder’s currency

vsmerchant’s currency

, I pick merchant’s. - If I’m unsure, I ask them to cancel and restart – I’d rather be awkward than pay 7.6% extra for nothing.

Takeaway: That friendly pay in your currency

button is usually a trap. For most travelers, local currency vs home currency is an easy choice: local currency almost always wins.

2. Choosing Your Travel Wallet: Cash, Card, or App?

Before you even leave home, you’re making the most important decision: which tools you’ll carry. Not just how much cash, but which cards and which apps.

Think of it as building a travel wallet with three roles:

- Main card for purchases – tap for flights, hotels, restaurants.

- ATM card for cash – pull out local currency when you need it.

- App or multi-currency account – to control when and how you convert.

Once you see it this way, the whole cash vs card when traveling abroad debate becomes less about either/or and more about using each tool for the right job.

Main card: credit or debit?

- Credit card (no foreign transaction fees)

Ideal for flights, hotels, car rentals, and big purchases. You get better fraud protection, sometimes travel insurance, and you’re not tying up your cash. The key line in the terms is no foreign transaction fees. Without that, every tap abroad quietly costs you extra. - Debit card (no foreign transaction fees)

Good for everyday spending if you hate credit or want to stick to a strict budget. Just remember: some hotels and car rentals strongly prefer credit cards for deposits, and fees for using a debit card abroad can add up if your bank isn’t traveler-friendly.

If your current card charges 2–3% on every foreign transaction, that’s like adding a permanent tax to your trip. On a $3,000 vacation, that’s $60–90 gone before we even talk about DCC or flight and hotel currency conversion charges.

Multi-currency apps and cards

Tools like Wise, Revolut and similar multi-currency accounts let you:

- Hold multiple currencies (EUR, GBP, JPY, etc.).

- Convert at or near the mid-market rate.

- Spend directly from those balances with a linked card.

Why this matters: you can choose when to convert. Maybe you move some money into euros months before your trip when the rate looks good. Maybe you convert in small chunks as you go. Either way, you’re not stuck with whatever rate your bank offers on the day.

For frequent travelers, travel money apps vs bank cards isn’t about loyalty to one side. It’s about using apps to dodge bad rates and keep control of your conversions.

Takeaway: Don’t rely on your everyday domestic card by default. Build a deliberate mix: one no-FX-fee credit card, one low-fee debit card for ATMs, and (optionally) a multi-currency app to decide when and how you convert.

3. ATMs Abroad: How to Get Cash Without Getting Fleeced

Cash is still unavoidable in many places – markets, small cafés, taxis, tips. The question isn’t cash or no cash?

It’s how do I get cash without paying 10% for the privilege?

Here’s the decision tree I use at ATMs when I want to avoid nasty foreign ATM withdrawal fees and surprise markups.

Step 1: Choose the right ATM

- Prefer bank-branded ATMs over random machines in tourist zones, hotels, or convenience stores.

- Avoid ATMs that scream

NO FEES!

in neon – they often hide the cost in terrible exchange rates.

Step 2: Watch for two separate costs

- ATM operator fee – a flat fee (e.g., $3–5) or a percentage. The machine usually shows this clearly.

- DCC markup – the sneaky one. The ATM offers to charge you in your home currency at a

guaranteed rate

.

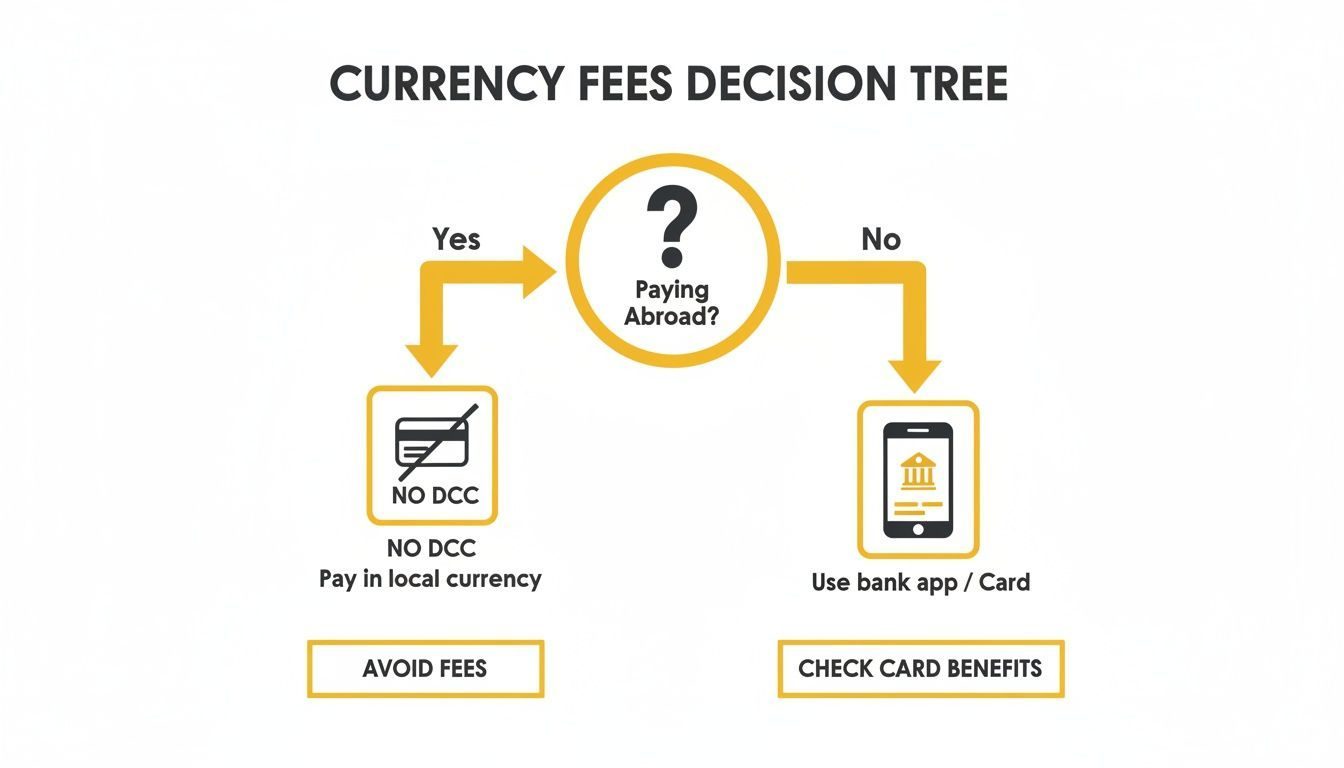

Decline the second one. Always.

When the ATM asks something like:

Convert to USD at 1 EUR = 1.02 USD?

Continue without conversion?

I hit continue without conversion. That tells the ATM to dispense local currency and let my bank handle the FX. It’s a simple way to avoid hidden currency conversion fees that get baked into bad rates.

Step 3: Withdraw smarter, not more

- If your bank charges a flat fee per withdrawal, it’s cheaper to take out larger amounts less often.

- If your bank charges a percentage, don’t over-withdraw and end up reconverting leftover cash at the end of the trip.

Takeaway: At ATMs, the most expensive button is usually the one that looks safest: charge in your home currency.

Say no, take local currency, and let your own bank convert. That one habit can save you more than any fancy travel money card marketing promise.

4. Flights, Hotels, and Big-Ticket Purchases: Where Small Percentages Hurt Most

It’s easy to shrug off a 3–7% fee on a coffee. It’s harder to ignore when you realize the same percentage applies to your $1,000 hotel bill or your $800 flight.

Let’s run a quick example.

You book a hotel abroad and pay at checkout. The bill is 1,000 in local currency. The terminal offers:

- Option A: Pay 1,000 in local currency

Your no-FX-fee card converts at the network rate. Let’s say you end up paying the equivalent of $1,000. - Option B: Pay in your home currency via DCC

The terminal shows $1,076 at aguaranteed rate

. That’s a 7.6% markup.

Same room. Same bed. Same breakfast. You just paid $76 extra for the privilege of seeing the number in your own currency.

Now imagine you repeat that mistake on:

- Flights

- Car rentals

- Resort bills

- Tour packages

Suddenly, you’ve tipped the system a few hundred dollars – not to staff, but to banks and payment processors. This is where currency conversion mistakes travelers make really sting.

How I handle big-ticket items

- Book in advance in my home currency when the price is fair and transparent (e.g., some airline sites, OTAs).

- Or book in the local currency if the site is clearly local and the rate is better – then pay with a no-FX-fee card.

- At the hotel front desk, I explicitly say:

Please charge me in local currency.

For the best way to pay for hotels abroad, that last line matters more than most loyalty programs.

Takeaway: The bigger the bill, the more dangerous DCC becomes. For flights, hotels, and packages, double-check the currency and refuse any guaranteed

conversion that isn’t from your own bank or app. That’s where you really save on exchange rates when traveling.

5. Airport Kiosks, Hotel Desks, and Other Currency Traps

You land, you’re tired, you just want a taxi. The first thing you see is a bright currency exchange booth promising NO COMMISSION

.

Here’s the uncomfortable truth: you pay either in fees or in the rate. Often both.

Airport and tourist-zone exchange booths

- They rarely give you the real market rate.

- They may advertise

0% commission

while quietly using a terrible rate. - In some places, there are stories of sleight-of-hand counting or old notes you can’t easily spend.

Does that mean you should never use them? Not necessarily. I sometimes exchange a small amount at the airport – just enough for transport and a snack – and then find a better option in the city.

Better alternatives

- Order some foreign cash from your bank before you leave, if the rate is reasonable.

- Use a bank ATM in the city, with a low-fee card, and decline DCC.

- Use your card directly for most purchases, again in local currency.

Think of airport kiosks as an emergency tool, not your main strategy. If you plan ahead, you won’t be forced into the worst possible international travel payment comparison at the worst possible moment.

Takeaway: The more desperate you feel when you see a currency booth, the more they can charge you. Plan for that moment in advance so you’re not negotiating with your jet-lagged self.

6. A Simple Playbook: How to Decide What to Use, When

Let’s pull this together into something you can actually use on the road. When I travel, I mentally run through a quick checklist every time I pay.

Step 1: What am I paying for?

- Flights, hotels, car rentals, big tours → use a no-FX-fee credit card.

- Restaurants, shops, everyday spending → credit or debit with no FX fees.

- Cash-only places → withdraw from a bank ATM with a low-fee debit card.

This is where the cash vs card when traveling abroad question becomes practical instead of theoretical.

Step 2: What currency is being shown?

- If it’s the local currency, I’m happy.

- If it’s my home currency while I’m abroad, I ask:

Is this DCC?

It usually is.

Step 3: Who is doing the conversion?

- If it’s my bank or my multi-currency app, I’m generally okay with it.

- If it’s a random merchant, hotel, or ATM offering a

guaranteed rate

, I’m suspicious.

Step 4: Can I avoid this conversion entirely?

- Sometimes I can pay directly from a local-currency balance in my app.

- Sometimes I can choose a different card with better terms.

- Sometimes I can just say

no

to DCC and let my bank handle it.

Takeaway: Every payment has three players – you, your bank, and the merchant’s bank. Your job is to keep control of who converts your money and when. That’s the heart of any smart international travel payment comparison.

7. Final Thoughts: Don’t Be Afraid to Be the Awkward Traveler

Most of these fees survive because we’re too polite, too rushed, or too tired to question them. We nod, we tap, we sign, and a few percent disappears.

On your next trip, try this instead:

- Ask your bank or card issuer about foreign transaction fees before you go.

- Practice saying:

Please charge me in local currency.

- Get comfortable declining

guaranteed

rates at ATMs and terminals. - Consider a multi-currency app if you travel often or to multiple countries.

You don’t need to obsess over every cent. But you also don’t need to tip the financial system 7–9% on every major purchase just to feel safe

. Once you understand dynamic currency conversion when you travel, it’s hard to unsee how expensive that comfort can be.

Travel is expensive enough. The goal isn’t to game the system – it’s simply to stop overpaying for the privilege of spending your own money.

Next time you’re standing at a terminal, finger hovering over home currency

or local currency

, remember: the cheapest option is rarely the one that feels most comfortable. It’s the one that quietly lets your own card network do its job – and keeps those hidden fees from nibbling away at your trip.