I used to hunt down flight deals and squeeze every point out of hotel programs, then tap my card abroad without thinking. Later, looking at my statements, I realized I’d quietly tipped 5–10% of my trip budget into bank profits and bad exchange rates.

The way you juggle cards, cash, and ATMs can quietly cost more than your flight.

This guide is for frequent travelers who want to stop overpaying on foreign transaction fees, weak exchange rates, and sneaky ATM charges. I’ll walk through the choices I make on every trip so you can build your own international travel money strategy—and keep more of your budget for the fun stuff.

1. How Much Cash Should You Land With?

The first money decision happens before you even leave home: How much local cash do I actually need when I land?

Here’s the trade-off:

- Too little cash → you’re forced into awful airport exchange rates or high-fee ATMs.

- Too much cash → you’re walking around with a theft magnet in your pocket.

After a lot of trips (and a lot of receipts), this is the rule of thumb that works for me:

- Card-friendly cities (e.g., London, Singapore, Stockholm): arrive with the equivalent of US$50–100 in local cash.

- Mixed or cash-heavy places (e.g., Japan outside big cities, parts of Southeast Asia, rural Europe): arrive with US$150–300 in local cash.

That usually covers:

- Airport transport (train, bus, taxi)

- Your first meal or snacks

- Tips, small shops, markets, public toilets, lockers

What I don’t do anymore:

- Airport exchange kiosks. Articles like this one show how airport counters often hide 5–10% (or more) in bad rates and commissions. You’re paying for convenience and the fact that you’re stuck.

- Exchanging my whole trip budget at home. Lose that envelope and your travel budget disappears. The rate at home is rarely the best either.

What works better for frequent travelers:

- Order a small amount of foreign cash online from a reputable provider before you go. Rates are usually better than walk-up airport counters, and you can pick up at a branch or airport.

- Use ATMs from major banks once you arrive for the rest of your cash (we’ll get into how to do that without getting crushed by international ATM fees).

Takeaway: Land with enough cash to avoid desperation exchanges, but not so much that losing your wallet wrecks the trip.

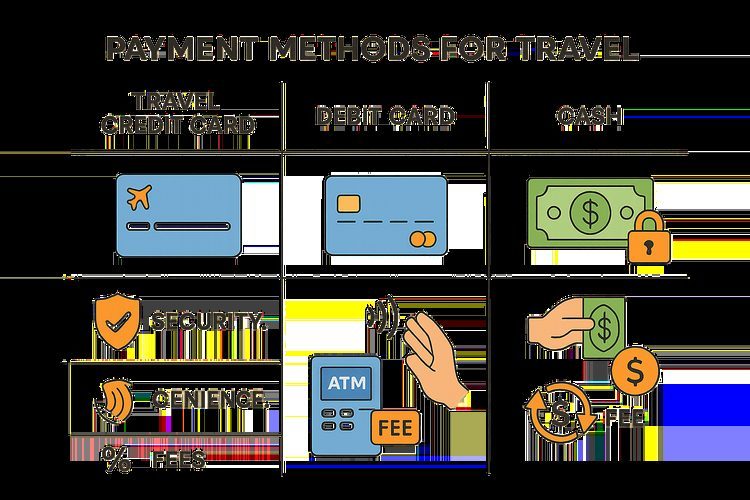

2. Credit Card vs Debit Card vs Cash: What Should You Use Most?

People often ask, What’s the single best way to pay abroad?

There isn’t one. But there is a smart mix that keeps costs down and stress low.

Here’s how I prioritize my travel banking day to day:

Credit cards: my default for purchases

For most purchases, I reach for a no-foreign-transaction-fee credit card. It’s my workhorse for international travel.

Why I lean on credit cards:

- Fraud protection. If someone skims your card, it’s the bank’s money at risk, not your rent. You dispute, they reverse.

- Rewards. Points, miles, or cashback can offset some of your travel costs over time.

- Security. Easy to freeze in the app if it’s lost or stolen.

- Tracking. Every transaction is logged, which makes post-trip budgeting and expense reports much easier.

But I’m picky about which card I use abroad:

- No foreign transaction fees. Many cards quietly add ~3% to every non-domestic purchase. That’s like a permanent extra tax on your trip.

- Visa or Mastercard first. Amex and Discover can be great at home, but acceptance abroad is hit-or-miss.

Debit cards: my tool for cash, not shopping

Debit cards shine at one thing: ATM withdrawals. Beyond that, I avoid using them for everyday spending unless I have no choice.

Why I limit debit card use for purchases:

- Weaker fraud protection. If your debit card is compromised, the money comes straight out of your bank account. You’ll usually get it back, but it can take time—and that can hurt while you’re still traveling.

- Stacked fees. Many banks charge both foreign transaction fees and ATM fees, which adds up fast.

What I look for in a travel debit card:

- No (or low) foreign transaction fees.

- ATM fee refunds or waivers. Some banks reimburse operator fees worldwide up to a certain cap.

- Visa or Mastercard network. For broad acceptance and smoother withdrawals.

Cash: essential, but limited

Even in tap-and-go cities, cash still matters more than many travelers expect.

I rely on cash for:

- Street food, markets, small cafés

- Tips and small services

- Rural areas and older businesses that don’t take cards

Cash has real advantages:

- No card fees. No foreign transaction fee, no dynamic currency conversion games.

- Budget control. A fixed daily envelope of cash makes overspending harder.

- Universal acceptance. Cash works when terminals don’t.

But the downsides are serious:

- Theft or loss. Once it’s gone, it’s gone.

- Exchange costs. You can still get hit with bad rates and commissions when you get that cash.

- No automatic record. Harder to see where your money went after the trip.

My mix on a typical trip:

- Credit card: 70–80% of spending (hotels, restaurants, transport, tickets).

- Cash: 20–30% (small purchases, tips, markets, rural areas).

- Debit card: mainly for pulling cash from ATMs at good rates.

Takeaway: For most frequent travelers, the sweet spot is a no-FX-fee credit card for everyday spending, a smart debit card for ATMs, and cash to cover the gaps.

3. The ATM Game: How to Withdraw Cash Without Bleeding Fees

ATMs can be the cheapest way to get cash overseas—or a quiet drain on your budget. The exchange rate is often better than at counters, but the fee stack can be brutal if you’re not paying attention.

When you withdraw abroad, you can face up to three separate costs:

- Your bank’s ATM fee (flat, percentage, or both).

- Exchange rate markup from your bank or card network.

- Local ATM operator fee (the machine owner’s cut).

Here’s how I keep those overseas card and ATM charges under control:

1. Choose the right ATM

- Prefer major bank ATMs. Use machines inside or attached to real banks, not random ATMs in convenience stores, hotels, or tourist strips.

- Avoid standalone tourist ATMs. These often have higher operator fees and aggressive dynamic currency conversion (DCC) prompts.

- Check for partner banks. Some banks have global alliances where foreign ATM fees are reduced or waived.

In many countries, bank ATMs have lower or no operator fees, while tourist-area machines quietly charge several dollars per withdrawal.

2. Make fewer, larger withdrawals

If your bank charges a flat fee per withdrawal, it’s usually cheaper to:

- Withdraw US$300 once than US$100 three times.

Of course, that means carrying more cash, so I adjust based on where I am:

- In safe, card-friendly cities: I withdraw smaller amounts more often.

- In high-fee countries or with a bank that charges per withdrawal: I take out more at once and use hotel safes or a money belt.

3. Always decline Dynamic Currency Conversion (DCC)

This is the big one. At many ATMs you’ll see something like:

We can charge you 10,000 JPY or 75.50 USD. Choose your currency.

Looks helpful, right? It isn’t.

Choosing your home currency (USD, EUR, etc.) is almost always more expensive. That’s DCC: the ATM or merchant sets a terrible exchange rate and pockets the difference. Articles like this one show how ugly those markups can be.

Rule: At ATMs and payment terminals, always choose to be charged in the local currency. Let your bank or card network handle the conversion.

4. Prep your card before you go

- Set a 4-digit numeric PIN. Many European ATMs won’t accept longer or alphanumeric PINs.

- Confirm international use with your bank. Ask how they handle fraud alerts and what to do if your card is blocked while you’re abroad.

- Keep most funds in your primary checking account. Some foreign ATMs only see the main account, not savings.

Takeaway: Use major bank ATMs, make fewer but larger withdrawals when it’s safe, and always decline DCC. Over a year of frequent travel, that alone can save you a surprising amount.

4. The DCC Trap: Why “Pay in Your Home Currency?” Is a Trick Question

If I could flip one global switch on every card terminal, I’d turn off Dynamic Currency Conversion forever.

You’ll see it when you pay by card or withdraw cash:

Pay 50.00 EUR or 54.90 USD?

We can convert this to your home currency for your convenience.

It sounds friendly. It’s not. Here’s what’s really going on behind that exchange rate fee choice:

- Local currency option: Your bank or card network (Visa, Mastercard, etc.) does the conversion, usually at a rate close to the mid-market rate, plus any foreign transaction fee your card charges.

- Home currency option (DCC): The merchant or ATM sets the rate. They often add a hidden markup of several percent on top of any fees you already pay.

So if your card already charges a 3% foreign transaction fee and you accept DCC with a 5% markup, you’ve just paid roughly 8% extra for that purchase. On a US$3,000 trip, that’s US$240 gone for nothing.

My rules at the terminal:

- If I see a choice of currencies, I always pick the local currency.

- If the screen is confusing, I look for the option that doesn’t mention my home currency or a

guaranteed rate

. - If a waiter or cashier helpfully selects my home currency, I politely ask them to switch it back to local.

Takeaway: When in doubt, pay in the currency of the country you’re standing in. Declining DCC is one of the easiest, highest-impact habits you can build to avoid hidden costs of using cards abroad.

5. Small Purchases: Tap the Card or Use Cash?

This is where a lot of people overpay without realizing it. That daily coffee, metro ticket, or snack can quietly rack up fees if your setup isn’t right.

Here’s how I decide between card and cash for small buys:

When I prefer cash for small buys

- My card has foreign transaction fees. Paying 3% extra on a US$3 coffee is silly if I already have cash I withdrew cheaply.

- High risk of card skimming. Tiny kiosks with ancient terminals, or places where the card disappears out of sight.

- Cash-based cultures. In some countries, small shops still prefer cash and may even give tiny discounts for it.

- Budget control days. If I’m trying to rein in spending, I’ll set a daily cash limit and stick to it.

When I’m happy to tap the card

- I’m using a no-FX-fee card. Then the cost difference between card and cash is minimal, and the convenience wins.

- Contactless is everywhere. In places like London or Singapore, tapping for transit and small purchases is fast and safe.

- I want a record. For business trips or expense reports, I prefer card transactions I can export later.

One subtle point: every time you use cash, you’re spending money you already paid to obtain (via ATM or exchange). If your international ATM fees are high, using your optimized credit card more and cash less can actually be the cheapest way to pay abroad.

Takeaway: If your card is fee-heavy, use cash for small purchases. If you’ve optimized your card (no FX fees, fair rates), tapping for small buys is usually fine—and often safer.

6. Building a “Travel Wallet” That Works in Almost Any Country

Instead of reinventing your setup for every trip, it’s worth building a simple travel wallet you can reuse and tweak. Think of it as your personal system for avoiding common banking mistakes for frequent travelers.

Here’s the core structure I use:

1. Primary credit card (no FX fees)

- Visa or Mastercard.

- No foreign transaction fees.

- Decent rewards (travel or cashback).

- Strong app for freezing/unfreezing and alerts.

This is my default for hotels, flights, restaurants, and most shopping. It’s the backbone of my travel banking cost strategy.

2. Backup credit card

- Different issuer/network from the primary (e.g., if primary is Visa, backup might be Mastercard or Amex).

- Ideally also no FX fees, but I’ll tolerate a small fee for backup.

I keep this card in a separate place (not in the same wallet) in case of loss, theft, or a random fraud block.

3. Travel-friendly debit card

- No or low foreign transaction fees.

- Low ATM withdrawal fees, or fee refunds.

- Good app controls and instant notifications.

This is my ATM workhorse. I rarely use it for purchases; I treat it like my cash pipeline and protect it accordingly.

4. Optional: multi-currency travel card

Services like Wise or Revolut (where available) can be useful for frequent travelers who want more control over exchange rate fees when traveling. They let you:

- Hold balances in multiple currencies.

- Convert at or near the mid-market rate.

- Lock in rates before a trip if you’re worried about currency swings.

I find these especially handy if I’m:

- Spending a lot of time in one currency (e.g., several months in Europe).

- Getting paid in foreign currencies.

5. Modest starter cash

As mentioned earlier, I usually aim for:

- US$50–100 equivalent for card-heavy destinations.

- US$150–300 equivalent for mixed or cash-heavy destinations.

Then I top up via ATMs as needed, using the same rules to avoid unnecessary overseas card and ATM charges.

Takeaway: Don’t rely on a single card or a fat wad of cash. A layered setup—primary card, backup card, smart debit card, and some cash—gives you resilience and keeps your travel banking cost down across different countries.

7. A Simple Pre-Trip Checklist That Can Save You Hundreds

To make this practical, here’s the checklist I run through before any international trip. It’s quick, and it’s saved me from a lot of foreign transaction fee mistakes.

- 1. Audit your cards.

- Which cards charge foreign transaction fees? (Plan to avoid them.)

- Do you have at least one no-FX-fee credit card for everyday spending?

- Does your debit card charge ATM fees abroad? Any fee refunds or partner banks?

- 2. Set up your PINs.

- Make sure your main cards have 4-digit numeric PINs.

- Test them at home before you go.

- 3. Call or chat with your bank.

- Confirm your cards will work in the countries you’re visiting.

- Ask how they handle fraud alerts and what to do if your card is blocked mid-trip.

- 4. Order a small amount of foreign cash.

- Enough for the first 24–48 hours: transport, food, small emergencies.

- Avoid exchanging large sums at airports.

- 5. Research ATMs at your destination.

- Which local banks are reputable and have fair fees?

- Are there known high-fee ATMs to avoid (especially in tourist zones)?

- 6. Install key apps.

- Your bank and card apps (for freezes, alerts, and PIN reminders).

- A currency converter (XE, OANDA, etc.) so you can sanity-check rates.

- 7. Decide your mix.

- Roughly what % of your spending will be card vs cash?

- How often will you withdraw from ATMs, given the fees?

Run through this once, then tweak it after a trip or two. You’ll end up with a personal system that quietly saves you money every time you leave the country—and turns banking for frequent travelers from a headache into a habit.

Final thought: You don’t need to be perfect. You just need to avoid the big, repeatable mistakes—airport exchanges, DCC, fee-heavy cards, and random tourist ATMs. Get those right, and you’ll keep hundreds of dollars a year in your own pocket instead of donating them to banks and kiosk operators.