I don’t plan trips assuming everything will fall apart. But I also don’t kid myself that the odds are in my favour anymore. Flights get cut, storms hit harder, airlines wobble, and medical care abroad can be brutally expensive. If you only budget for flights and hotels, you’re playing financial roulette with the hidden costs of travel disruptions.

In this guide, I’m walking through the real costs of disruption—delays, cancellations, missed connections, and medical surprises—and how to budget for them without doubling your trip price. Think of it as a personal disruption fund, not a fear-based checklist. You’re planning for the likely, not the apocalypse.

1. The New Normal: Why Disruptions Are No Longer “Bad Luck”

Here’s the uncomfortable bit: travel disruptions aren’t rare anymore. They’re baked into the system.

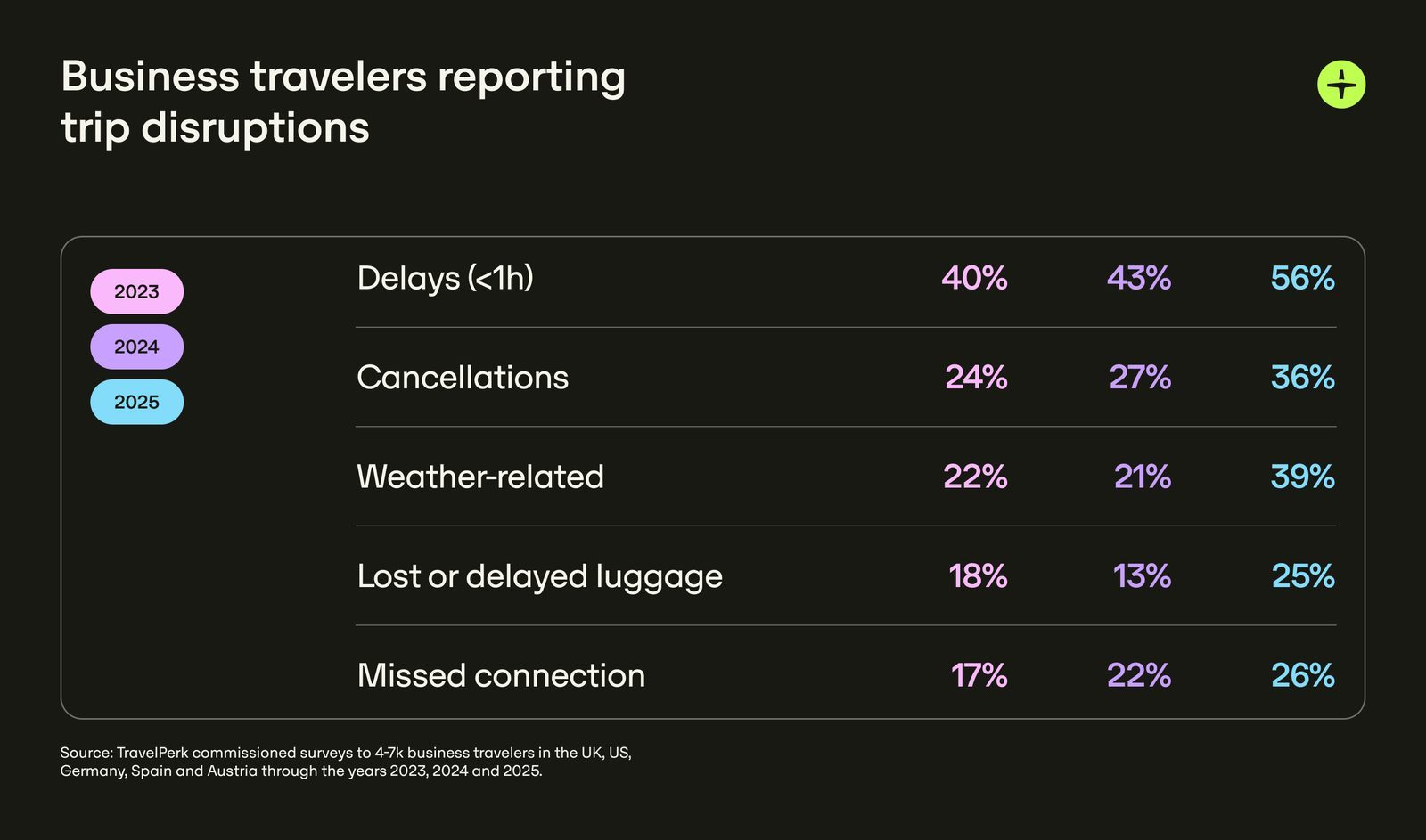

Airlines are trimming routes, cutting summer schedules, and quietly cancelling flights weeks in advance to dodge compensation rules. Some carriers are collapsing outright, leaving passengers stranded and scrambling to rebook at walk-up prices. One global survey of business travellers found that 89% experienced disruptions in a single year—up from 77% just two years earlier. That’s not bad luck. That’s the baseline.

Weather is more volatile. Airspace closures and tech outages are more common. Visa rules shift with little warning. Airlines run leaner schedules with almost no slack. When one thing breaks, it cascades.

So on any trip, I assume three things:

- At least one leg may be delayed by an hour or more.

- One major disruption—a cancellation, missed connection, or serious delay—is plausible on multi-leg or long-haul trips.

- Medical care abroad won’t be priced like home, and my regular insurance may not follow me.

Once you accept that, the question shifts from Will something go wrong?

to How much am I willing to pay if it does?

That’s where travel disruption financial planning starts to matter.

2. The Real Price of a Delay: Time vs Money

On paper, a delay looks harmless. An extra hour or two in the airport. A bit of boredom. No big deal, right?

In reality, the hidden costs of travel disruptions show up fast.

From that same business travel survey, 56% of travellers reported delays over an hour. Around 40% ended up paying extra out of pocket—mostly for accommodation and overtime. US companies alone burn over $17 billion a year on disruption-related extras. That’s not just a corporate problem; it’s a warning sign for personal travellers too.

Here’s how I break down delay costs when I budget for flight delays and cancellations:

- Food & drinks: Airport prices are often 2–3x normal. One long delay can easily mean $30–$60 per person in snacks and meals.

- Ground transport: Missed trains, late-night taxis, rideshares when public transport shuts down, or extra trips back and forth.

- Overtime & lost income: If you’re self-employed or freelance, a lost workday is a real cost, even if it doesn’t show up on your credit card.

My rule of thumb for delays:

- For short trips (3–5 days), I set aside the equivalent of one extra travel day in my budget: food, local transport, and a small buffer.

- For longer or complex trips, I assume at least one major delay and build a flat disruption buffer (more on that later).

And I don’t just budget money. I budget time. I book earlier flights, longer layovers, and avoid razor-thin connections. It feels overly cautious—until you’re the one calmly boarding your backup flight while everyone else is sprinting through the terminal.

3. Cancellations & Airline Chaos: How Much Risk Are You Really Taking?

Cancellations are where the big money leaks out. Not because your original ticket vanishes, but because you’re forced into last-minute decisions at premium prices.

Globally, about 36% of travellers reported cancellations in a recent year, up from 24%. In the US, it’s even worse. Flights account for most of those cancellations, and when airlines cut routes or collapse entirely, you’re suddenly shopping for new tickets in a seller’s market.

Meanwhile, airlines are squeezed by fuel costs and thin margins. Some trim schedules. Others quietly cancel flights more than two weeks out to avoid paying compensation. A few simply shut down, hand back their licences, and leave passengers holding worthless tickets.

So how do you handle the cost of missed connections and rebooking without over-insuring everything?

I start with three questions:

- Is my ticket flexible? Non-refundable, basic economy, or heavily restricted fares are cheaper upfront but brutal when plans change.

- How critical is this trip? If missing it means losing a big client, a once-in-a-lifetime event, or a non-refundable tour, I treat it differently.

- What’s my Plan B? Could I take a train, drive, or reroute through another city if my main flight disappears?

Then I choose between three strategies:

- Pay more for flexibility. A slightly higher fare with low or no change fees. Often cheaper than paying for last-minute rebookings when things go wrong.

- Self-insure with a disruption fund. I accept the risk of a non-refundable ticket but keep a dedicated pot of money for emergencies.

- Use targeted travel insurance. Especially when I’ve prepaid non-refundable tours, cruises, or packages and want help with travel delay and cancellation insurance costs.

What I don’t do is pretend a rock-bottom fare is “cheap” if it only works in a perfect world. It’s not. It’s a bet. And I only place that bet when I’m willing to lose.

4. The First Six Hours: Your Personal Crisis Playbook

When a major disruption hits—mass cancellations, airspace closures, tech outages—the first six hours decide whether you bleed money or stay in control.

I treat those hours like a checklist, not a panic spiral. You don’t need to predict every scenario; you just need a plan.

Here’s the playbook I use:

- Avoid the longest queue in the airport. Service desks look comforting, but during mass disruptions they’re usually the slowest option. Airline apps and websites often process rebookings faster and at scale.

- Secure shelter early. If it looks like you’ll be stuck more than four hours—especially late in the day—I start looking for hotels within 60–90 minutes. Nearby hotels sell out fast. I’d rather book a cancellable room and release it than sleep on the floor.

- Use your own money strategically. Sometimes booking your own hotel or alternative transport and claiming later is faster and cheaper than waiting for the airline to organise anything. But I only do this after reading the airline’s disruption policy and taking screenshots.

- Protect your connectivity. Without data, you’re stuck in the 1990s. I always have a roaming plan, eSIM, or local SIM option ready so I can rebook, check policies, and contact support on the move.

- Document everything. Boarding passes, delay notices, receipts, screenshots of app messages. If I need to claim compensation or insurance later, this is my evidence.

The focus is simple: shelter, communication, documentation, rerouting. That’s your personal emergency travel budget planning in action.

5. Medical Surprises: The Most Dangerous Line Item to Ignore

Delays and cancellations are annoying. Medical surprises can be financially catastrophic.

Many travellers assume their regular health insurance follows them abroad. Often it doesn’t—or it does, but with limited networks, high deductibles, or no coverage for evacuation. A simple clinic visit might be manageable. A hospital stay or emergency evacuation can run into tens or hundreds of thousands.

This is where I’m least willing to gamble. Unexpected travel medical expenses are the one category that can blow up even the best disruption budget.

Here’s how I think about medical risk:

- Destination matters. A sprained ankle in a country with affordable care is one thing. A serious injury in a remote area or a country with high private healthcare costs is another.

- Trip style matters. City break vs. trekking, diving, skiing, or adventure travel. The more physical the trip, the more I care about evacuation coverage.

- Existing coverage matters. I check whether my home insurance covers international emergencies, what the limits are, and whether evacuation is included.

When I decide to buy travel medical coverage, I don’t just click the first checkbox. I compare plans—often through a marketplace like InsureMyTrip—and look for:

- Emergency medical limits high enough to cover a serious hospital stay.

- Evacuation coverage to get me to a proper hospital or back home if needed.

- Pre-existing condition clauses and how they’re handled.

Typical travel insurance runs about 4–10% of the trip price. I don’t buy it for every weekend away. But for international trips, expensive itineraries, or anything involving riskier activities, I treat it as a core part of the budget, not an optional extra. That’s how I handle budgeting for travel medical surprises without losing sleep.

6. Building a Disruption Budget: How Much Extra Should You Actually Set Aside?

Let’s get concrete. How much should you actually set aside for the extra costs of being stranded during travel?

Vague advice like “add a buffer” doesn’t help much. I prefer a simple framework I can tweak per trip—a practical travel disruption cost breakdown.

Step 1: Start with your core trip cost.

- Add up flights, trains, accommodation, and major prepaid activities.

Step 2: Add a disruption buffer as a percentage.

For most trips, I use this range:

- Low-risk, domestic, simple trips: +5–7% of total trip cost.

- International or multi-leg trips: +8–12%.

- Complex, high-stakes, or peak-season trips: +12–15%.

This buffer covers things like:

- Extra meals and airport spending during delays.

- Last-minute ground transport (taxis, rideshares, replacement trains).

- One unplanned hotel night.

- Change fees or partial rebooking costs.

Step 3: Decide what you’ll self-insure vs. outsource.

- If I’m self-insuring, I keep that buffer in cash or a separate account and accept that I’ll pay out of pocket if things go wrong.

- If I’m using insurance, I still keep a smaller buffer for upfront costs (you often pay first and claim later).

Step 4: Align your bookings with your buffer.

There’s no point buying the cheapest, least flexible ticket if your disruption buffer is tiny. Either:

- Pay more upfront for flexibility and reduce your buffer, or

- Pay less upfront and increase your buffer, accepting more risk.

The key is making a conscious trade-off, not just chasing the lowest headline price and hoping for the best. That’s how you avoid the most common travel budgeting mistakes for disruptions.

7. Business Travel: When Hidden Costs Hit the Company Card

If you travel for work, the stakes are different. The company might be paying, but the disruption still hits you in stress, time, and sometimes your reputation.

Corporate travel budgets are often blown not by headline items like flights and hotels, but by hidden costs such as:

- Change fees and cancellation penalties from last-minute itinerary shifts.

- Unused tickets that never get rebooked or refunded.

- Employees booking outside approved channels, making spend harder to track.

- Ground transport chaos when flights are delayed or diverted.

Some companies respond by locking everything down with rigid, lowest-fare-only policies. That looks good on paper and terrible in real life. Non-refundable tickets and tight connections might save a few dollars upfront but explode costs when disruptions hit.

If I were designing a resilient business travel policy, I’d push for:

- More flexible fares on critical routes, especially for high-frequency travellers.

- Clear guidelines on flight timing: earlier departures, longer layovers, and avoiding last flights of the day when possible.

- Centralised booking and ground transport tools so travellers can adapt quickly (and within policy) when plans change.

- Analytics to track where change fees and disruption costs are actually coming from.

Disruptions don’t just cost money. They cost opportunities. About a quarter of business travellers believe they’ve missed new business because of travel chaos. Two-thirds report higher stress and worse work-life balance. That’s not just a travel problem; it’s a talent problem.

8. Putting It All Together: Your Personal Disruption Strategy

Here’s the mindset I carry into every trip:

- Assume disruption is normal. Not every trip will melt down, but enough will that it’s worth planning for.

- Decide your risk tolerance upfront. Are you okay with non-refundable everything, or do you sleep better with flexibility and insurance?

- Build a realistic disruption budget. Aim for 5–15% of your trip cost, depending on complexity and stakes.

- Have a crisis playbook. In the first six hours: rebook digitally, secure shelter, protect connectivity, document everything.

- Don’t ignore medical risk. International travel medical emergency costs are the one category that can truly wreck your finances.

You don’t need to be paranoid. You just need to be deliberate. The goal isn’t to eliminate all risk—that’s impossible. The goal is to make sure that when the next delay, cancellation, or medical surprise hits, it’s an inconvenience, not a financial disaster.

So next time you plan a trip, ask yourself: If this goes sideways, how much am I really willing to pay?

Then build your budget—and your strategy—around that honest answer. That’s your personal cost guide for travel emergencies.