I’ve lost more money to bad exchange rates and sneaky fees than I care to admit. Not because I was reckless, but because I didn’t know the rules of the game. Banks, ATMs, and payment processors all take their cut. If you don’t plan, you pay.

This guide is how I travel now: a simple, flexible money setup that works in most countries, avoids the worst fees, and still keeps me covered when things go wrong.

Core idea: don’t pick cash vs. card vs. apps. Build a layered money stack

that uses all three on your terms, not the bank’s. That’s how you avoid the classic cash vs card abroad debate and actually build a real travel money strategy overseas.

1. Start With the Big Question: What Do You Actually Need Your Money to Do?

Before you obsess over which travel card or payment app is best, zoom out. Your money has to do four jobs every time you leave home:

- Pay for big, bookable stuff – flights, hotels, trains, tours.

- Cover daily life – food, metro, coffee, museum tickets.

- Handle cash-only moments – markets, taxis, tips, public toilets, rural areas.

- Survive a mini-disaster – card gets cloned, wallet stolen, app locked.

Most people only plan for the first two. That’s how you end up stranded at a rural bus station with a dead card and no cash.

Here’s the mindset shift that changed things for me:

- Cards = convenience, rewards, and protection.

- Cash = resilience and control.

- Apps / multi-currency cards = flexibility and lower FX costs.

Your job is to decide how much of each you need for this trip, not in theory.

City break in London or Singapore? You can go card-heavy and lean on contactless payments. Road trip in the rural Balkans or parts of Latin America? You’ll want a more cash-heavy setup. Backpacking Southeast Asia on a tight budget? Think apps + ATMs + a bit of USD or EUR as backup.

Takeaway: don’t ask Is cash or card better?

Ask: What mix of cash, cards, and apps fits the way I’m actually traveling?

That’s the real cash vs card vs apps when traveling question.

2. The Card Trap: How to Use Credit & Debit Abroad Without Bleeding 3–10%

Cards are usually the smartest way to pay abroad if you pick the right ones and use them correctly. Get it wrong, and you quietly lose 3–10% on almost every transaction. That’s a painful way to fund your bank’s profits.

Step 1: Audit the cards you already have

Before you apply for anything new, log into your accounts and check:

- Foreign transaction fee? Often 2–3% on every non-home-currency purchase. This is one of the most common foreign transaction fee mistakes.

- Network? Visa and Mastercard are safest globally; Amex and Discover can be hit-or-miss.

- Chip + contactless? Many countries rely on EMV chip and tap-to-pay. Magstripe-only cards can fail at ticket machines and shops.

If your main card charges foreign transaction fees, you’re starting every purchase in the red. On a $3,000 trip, 3% is $90 gone for nothing.

Step 2: Get a no-foreign-transaction-fee card (if you can)

Ideally you want:

- No foreign transaction fees

- Good rewards on travel & dining

- Solid fraud protection

Sometimes these cards have annual fees. Don’t reject them automatically. Do the math:

- If you’d pay $120/year but save $90 in FX fees and earn $150 in rewards, the fee is effectively covered.

If you only travel every few years, a no-fee, no-FX card might be better, even with weaker rewards. The goal is the cheapest way to pay in foreign currency for your travel pattern, not in theory.

Step 3: Use credit vs. debit strategically

- Credit card for: flights, hotels, car rentals, restaurants, online bookings. You get better fraud protection, chargeback rights, and often rewards.

- Debit card for: ATM withdrawals only, ideally from low-fee or fee-refunding banks.

Why not use debit everywhere? Because if something goes wrong, it’s your actual money at risk, not the bank’s. With credit, disputes are usually easier and your cash flow isn’t frozen while the bank investigates.

Takeaway: for a smart credit card vs debit card abroad costs setup, carry one no-FX-fee credit card for spending, one low-fee debit card for ATMs, and leave the rest at home.

3. Cash Abroad: How Much, When to Get It, and How Not to Get Ripped Off

Cash is annoying until you really need it. Then it’s priceless.

When cash still wins

Even in card-heavy countries, I still use cash for:

- Street food, markets, and small family-run shops

- Taxis, local buses, and some trains

- Tips for guides, hotel staff, and drivers

- Public restrooms (especially in Europe)

- Rural areas with weak internet or power cuts

In some places, paying cash can even get you a small discount because the merchant avoids card fees. It’s worth asking: Is the price different for cash?

How much cash should you carry?

Everyone’s risk tolerance is different, but here’s a simple starting point:

- Enough for 1–2 days of expenses in your wallet.

- Another 2–4 days’ worth hidden in your bag or hotel safe.

That’s usually enough to handle card outages, ATM issues, or a lost card without walking around with a robbery-sized wad of notes. If you’re wondering how much cash to carry when traveling, this rule of thumb works in most places and you can adjust up or down based on how remote you’re going.

Where to get cash without getting fleeced

- Avoid airport kiosks and hotel exchanges. Their rates can be 10–15% worse than the real rate.

- Use ATMs at real banks, not random tourist machines in bars or souvenir shops.

- Withdraw larger, less frequent amounts to spread fixed ATM fees over more cash.

If you like to land with some local cash in hand, consider ordering a small amount from a reputable provider at home rather than exchanging at the airport. You’ll rarely get a perfect rate, but you’ll avoid the worst of it.

Takeaway: cash is your safety net and your budget anchor. Don’t overdo it, but don’t skip it either.

4. The Silent Killer: Dynamic Currency Conversion (DCC) and Bad Exchange Rates

If you remember only one thing from this article, make it this:

Always pay in the local currency, never in your home currency.

That moment at the card terminal when it asks:

Pay 50.00 EUR or 55.20 USD?

Choosing USD (or your home currency) feels safer. It’s not. That’s Dynamic Currency Conversion (DCC), and it’s almost always a bad deal.

Why DCC is so expensive

- The merchant or ATM sets the rate, not Visa or Mastercard.

- They bake in a fat markup, often 5–7% or more.

- You may still pay your bank’s foreign transaction fee on top.

So you’re paying extra for the privilege of seeing a familiar currency on the screen. It’s one of the easiest dynamic currency conversion traps to fall into.

What to do instead

- At shops and restaurants: say “charge me in local currency”.

- At ATMs: if it offers to convert to your home currency, decline conversion.

- If a cashier insists there’s no choice, I’ll often walk away unless I truly have no alternative.

Combine this with a no-foreign-transaction-fee card and you’re suddenly paying very close to the real mid-market rate. That’s the backbone of any overseas spending strategy for travelers.

Takeaway: DCC is optional. You just have to be alert enough to say no.

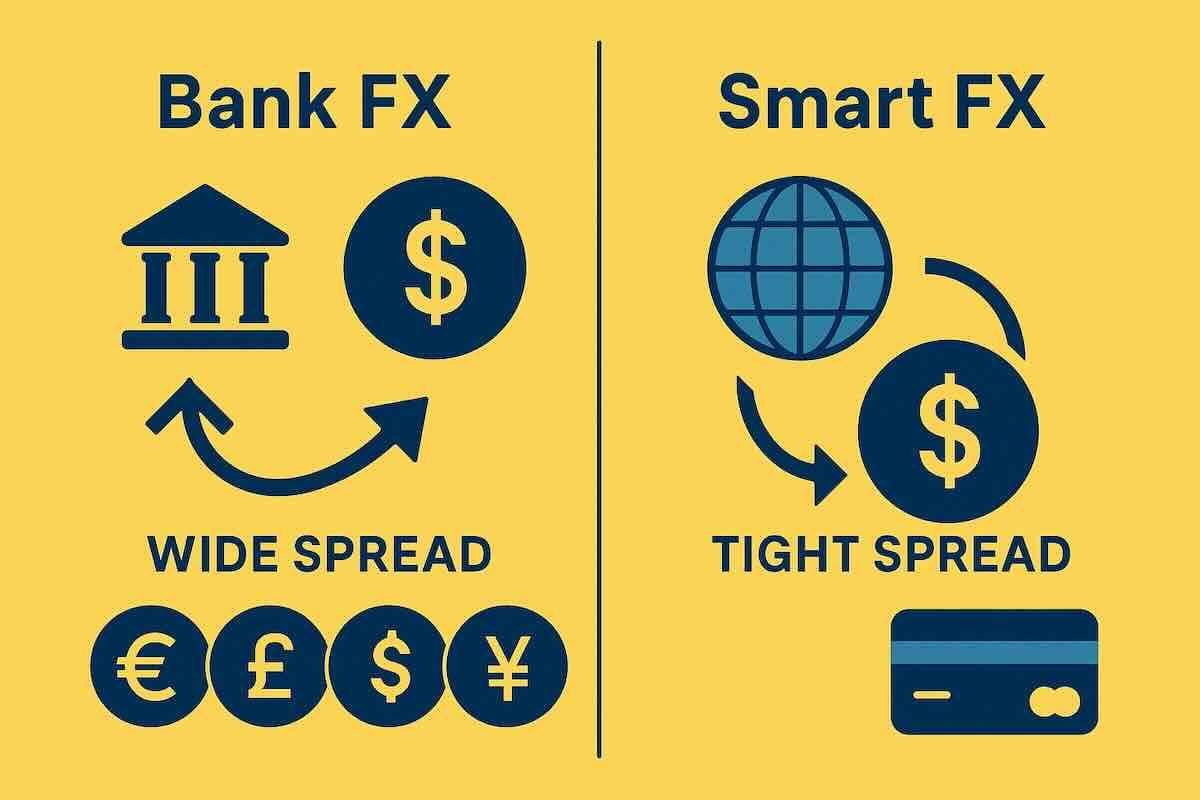

5. Payment Apps & Multi-Currency Cards: When They Beat Your Bank (and When They Don’t)

Payment apps and multi-currency cards (Wise, Revolut, and similar tools) promise better exchange rates and slick budgeting. Sometimes they deliver. Sometimes they just move the fees around and hide them in new places.

Where these apps shine

- Better FX rates than many traditional banks, often close to the mid-market rate.

- Multi-currency balances – you can hold EUR, GBP, JPY, etc., and spend like a local.

- In-app controls – freeze cards, set limits, get instant notifications.

- Budgeting – separate your travel money from your main accounts.

For long trips or multi-country itineraries, this can save real money and mental bandwidth. They’re especially handy if you’re comparing different travel cards and payment apps and want one place to track everything.

But read the fine print

These tools are not magic. Watch for:

- Top-up fees (especially with credit cards).

- ATM withdrawal limits before extra charges kick in.

- Weekend or off-hours FX markups.

- Account verification delays – not fun if your account gets frozen mid-trip.

Also, in some countries (China is the classic example), local payment ecosystems rely heavily on QR-based apps. Your Western card might technically work, but the path of least resistance is often to plug your card into a local-friendly wallet.

Takeaway: apps and multi-currency cards are powerful tools, but they’re not a replacement for a solid card + cash base. Treat them as an upgrade to your travel money strategy overseas, not a crutch.

6. ATM Strategy: How to Pull Out Cash Without Donating Half to the Banks

ATMs are usually the cheapest way to get local cash. They’re also where a lot of travelers quietly bleed money through international ATM withdrawal fees and bad rates.

Know the three layers of ATM cost

- Your bank’s fee for using a foreign ATM.

- The local ATM’s fee (often disclosed on-screen).

- The exchange rate markup if DCC is involved or your bank uses a poor rate.

On a long trip, this can add up to hundreds of dollars.

How to minimize ATM pain

- Use a bank that refunds ATM fees or belongs to a global ATM alliance, if available in your country.

- Withdraw more, less often – one $300 withdrawal with a $5 fee is better than three $100 withdrawals with $5 each.

- Stick to ATMs attached to real banks during business hours when possible.

- Decline any on-screen conversion and choose to be charged in local currency.

And always have a backup: if your main debit card fails, you don’t want your entire cash strategy to collapse.

Takeaway: ATMs are your friend if you pick the right card, the right machine, and the right withdrawal pattern. That’s a big part of the best way to pay abroad to avoid fees.

7. Risk Management: What Happens If Your Wallet Vanishes?

This is the part most people skip. It’s also the part that decides whether a bad day becomes a full-blown travel nightmare.

Split and separate

I never keep all my money in one place. My usual setup:

- On me: main credit card, day’s cash, maybe a transit card.

- In the room safe / hidden in luggage: backup credit card, backup debit card, extra cash.

- In the cloud: photos of cards (front only), passport, and emergency numbers stored securely.

If my wallet disappears, I can still:

- Cancel cards quickly.

- Access backup cards.

- Pay for a few days while replacements are arranged.

Set up alerts and controls

Before you go, turn on:

- Transaction alerts for your cards.

- App access so you can freeze and unfreeze cards instantly.

Fraud is much easier to handle when you catch it early. This is one of the simplest ways of avoiding hidden travel payment fees from unauthorized charges.

Takeaway: assume something will go wrong. Design your money setup so it’s an inconvenience, not a crisis.

8. Build Your Personal Travel Money Blueprint

Now let’s turn this into something you can actually use. Grab a piece of paper (or your notes app) and answer these, honestly:

- Where am I going, and how card-friendly is it? Big cities vs. rural areas, Europe vs. cash-heavy regions.

- How long am I going for? Weekend, two weeks, months?

- What’s my total budget? Rough numbers are fine.

- What cards do I already have? Note which charge foreign transaction fees.

- How comfortable am I with cash? Some people love it for budgeting; others hate carrying it.

Now build your stack – your personal travel cost guide for payments in action:

- Primary card: no-FX-fee credit card for most purchases.

- Secondary card: another network (e.g., Visa + Mastercard) stored separately.

- ATM card: low-fee debit card, ideally with fee refunds.

- Cash: small amount in home currency + 1–2 days of local currency on arrival, then top up via ATMs.

- Optional app: multi-currency or travel card if you’re visiting multiple countries or want tighter budgeting and clearer visibility into payment apps abroad fees.

Layer on the rules:

- Always pay in local currency.

- Decline DCC at terminals and ATMs.

- Withdraw cash in larger, less frequent chunks from bank ATMs.

- Split your cards and cash between your person and your luggage.

If you do just that, you’re already ahead of most travelers. You’ll still pay some fees – nobody gets to zero – but you’ll stop leaking money on the dumb, avoidable ones.

And that’s the point: more of your travel budget going to experiences, less to bank profits.