I’ve lost more money to bad exchange rates and sneaky bank fees than I care to admit. Not because I was reckless, but because I didn’t know where the traps were.

If you’re about to travel, the real question isn’t just cash or card?

It’s: what mix of cash, cards and mobile wallets actually works out cheapest abroad once you factor in exchange rates, ATM charges, foreign transaction fees and dynamic currency conversion (DCC) markups.

Let’s walk through the key decisions one by one, so you can build a simple, low‑fee setup that works almost anywhere.

1. How Much Cash Should You Take – and When Is It Actually Cheaper?

First decision: how much physical cash do you really need? Too little and you’re stuck at a terrible airport kiosk. Too much and you’re carrying a brick of money you’re scared to lose.

Here’s how I think about it now when I’m weighing cash vs card abroad fees:

- Always land with some local cash. Enough for the first 24 hours: airport transport, a meal or two, tips, a SIM card, small shops. For many trips, that’s the equivalent of US$50–150.

- Order ahead, don’t buy at the airport. Airport kiosks often bake in a 5–10%+ margin. Online FX services or your bank’s pre-order desk usually give you a much tighter rate (as noted in this guide).

- Use ATMs for the rest. In most countries, a bank ATM will beat a walk-up exchange booth on rate, even after a modest fee.

Cash is still king for:

- Street food, markets, small family-run places

- Taxis and local buses (especially outside big cities)

- Tipping guides, hotel staff, drivers

- Cash-first cultures (think rural areas, traditional inns, some parts of Asia)

But cash has a hidden cost: you pay the FX margin upfront on the whole amount, whether you spend it or not. Leftover currency on the way home? You’ll pay another spread to convert it back.

My rule now: enough cash to be comfortable, not enough to be annoying. I top up at ATMs in larger, less frequent withdrawals to dilute fixed overseas ATM withdrawal charges.

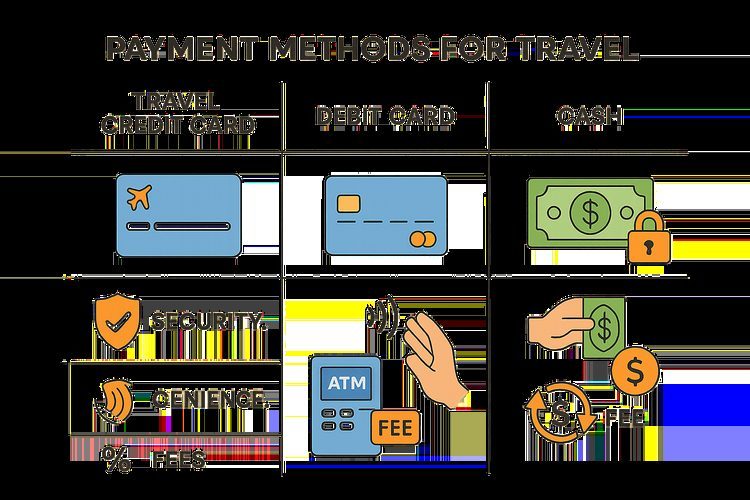

2. Debit vs Credit Card Abroad – Which One Should You Actually Use?

Most of us already have both a debit and a credit card. The expensive mistake is using the wrong one for the wrong job.

Here’s the simple split I use now (and that many travel experts recommend when they explain international card fees):

- Credit card for purchases (hotels, restaurants, tickets, online bookings)

- Debit card for ATM withdrawals (to get local cash)

Why credit cards win for spending:

- Better protection. Fraud on a credit card is the bank’s money first, not yours. Disputes are easier and you’re not locked out of your rent money while they investigate.

- Rewards and perks. Travel cards often give points, insurance, rental car coverage and lounge access. That can offset fees if you use them smartly.

- Competitive FX rates. Visa/Mastercard rates are usually close to market; the real killer is the foreign transaction fee (often 2–3%) layered on top.

Why debit cards are best for cash:

- Direct access to your money. No cash advance interest, no credit limit games.

- Good base rates. Network FX rates again are usually decent.

- But watch the fees. Your bank may charge an international ATM fee, plus the local ATM operator may add their own. That’s why larger, less frequent withdrawals are usually cheaper.

The big risk with debit: if your card is skimmed, your actual bank balance is hit. Recovery can be slow and stressful. That’s why I never use my main debit card for everyday purchases abroad – only at ATMs, and preferably at machines attached to real banks.

So the working formula for the cheapest way to pay abroad most of the time:

- Credit card (no FX fee if possible) → day-to-day spending

- Debit card (low ATM fees) → cash top-ups

3. The Silent Killer: Foreign Transaction Fees & Dynamic Currency Conversion

This is where most people quietly bleed money.

Two separate costs are at play when you tap your card abroad:

- Foreign transaction fee – usually 1–3% per purchase, charged by your bank/issuer and sometimes the network.

- Dynamic currency conversion (DCC) – the

Do you want to pay in your home currency?

trick at terminals and ATMs.

They’re different – and you want to avoid both if you’re trying to avoid foreign transaction fees and nasty surprises.

Foreign transaction fees:

- Often around 3% total (about 1% network + 2% issuer is common, as explained in this breakdown).

- Show up as a separate line on your statement or baked into the FX rate.

- Apply not just abroad, but also when you buy online from foreign merchants.

DCC (Dynamic Currency Conversion):

- That moment when the terminal says:

Pay 50 EUR or 55 USD?

- Paying in your home currency looks friendly, but the rate is usually awful – markups of 7% or more are common.

- Merchants or ATM operators set the rate, and they set it to favor themselves.

My rule is non-negotiable now: always choose to pay in the local currency. When you’re given a choice between local currency vs home currency payment, local wins almost every time.

If the machine defaults to your home currency, I cancel and start again. If a waiter presses the wrong button, I ask them to void it and redo it in local currency.

And yes, sometimes DCC is added without asking. I check receipts and statements and dispute any unauthorized DCC with the card issuer. It’s tedious, but it’s my money.

![Guide to Credit Card Foreign Transaction & Currency Conversion Fees [2026]](/static/images/img_a10853a7.jpg)

4. Are Multi‑Currency & Prepaid Travel Cards Worth It?

Wise, Revolut, Travelex and other multi-currency cards are everywhere now. Are they actually cheaper, or just another shiny product?

Used well, they can be powerful and sometimes beat traditional banks in a travel money cost comparison:

- Lock in rates in advance. You can convert a chunk of money into EUR, JPY, etc. when rates look good, and then spend from that balance.

- Often lower FX margins. Many of these cards use near-mid-market rates with a small, transparent fee.

- Budget control. You can load a fixed amount and avoid accidentally overspending your main account.

But there are catches:

- Fee complexity. Some charge for loading, inactivity, ATM withdrawals, or for using the card in a currency you haven’t preloaded.

- Acceptance. They usually run on Visa/Mastercard rails, but some merchants and hotels are picky about prepaid cards for deposits.

- Over-hedging. If you load too much in one currency and don’t spend it, you’ll pay again to convert it back.

When do I like them?

- Trips where I know I’ll spend a lot in one or two currencies.

- Longer stays where budgeting tightly matters.

- As a primary travel card with a traditional credit card as backup.

When do I skip them?

- Short trips with modest spend.

- When I already have a no-FX-fee credit card and a low-fee debit card.

If you do use one, treat it like a mini travel bank account: understand every fee, keep the app installed, and don’t leave big balances sitting there long after the trip.

5. Mobile Wallets (Apple Pay, Google Pay, etc.) – Cheaper or Just Easier?

Mobile wallets feel futuristic, but the key question is simple: do they save you money?

In most cases, the answer is: not directly. When you tap your phone, you’re still using the underlying card. The FX rate and foreign transaction fees are the same as if you’d used the plastic.

So why bother using mobile wallet international payments at all?

- Security. Your card number is tokenized. If your phone is stolen, you can wipe it remotely. That’s often safer than losing a physical wallet.

- Convenience. No fumbling for cards, especially in cities where contactless is the norm.

- Less card wear. Fewer chances for your physical card to be skimmed or damaged.

The downsides:

- Acceptance varies. In some countries, mobile wallets are everywhere. In others, you’ll get blank stares.

- Battery dependence. Dead phone, dead wallet. I never rely on it as my only method.

My approach: I add my best travel credit card (no FX fee, good rewards) to my mobile wallet and use that combo wherever it’s accepted. But I always carry at least one physical backup card and some cash.

6. ATM Strategy: How to Pull Out Cash Without Getting Fleeced

ATMs can be your best friend or your most expensive habit abroad. The difference is in how you use them.

Here’s the playbook I follow now to keep overseas ATM withdrawal charges under control:

- Use bank ATMs, not tourist machines. I look for ATMs physically attached to banks, not the bright standalone ones in tourist zones with huge

0% commission

signs. - Withdraw more, less often. If each withdrawal costs a fixed fee (say $3–5), taking out the equivalent of $200–300 at a time usually beats lots of small withdrawals.

- Always choose local currency. If the ATM offers to charge you in your home currency, that’s DCC again. I decline it every time.

- Know your bank’s policy. Some banks refund international ATM fees or have partner banks abroad. Others gouge you. I check this before I fly.

I also keep a mental checklist:

- Is the ATM in a well-lit, secure area?

- Does the card slot look tampered with?

- Is the fee clearly shown before I confirm?

If anything feels off, I walk away. There’s almost always another ATM within a few blocks.

7. Building Your Personal, Low‑Fee Travel Money Setup

Let’s turn all of this into a simple, practical setup you can actually use. Think of it as your personal system to reduce bank fees abroad and dodge the usual travel money mistakes.

Before you go, I’d do this:

- Audit your cards. For each card, check:

- Foreign transaction fee (0% is ideal)

- ATM fees (domestic and international)

- Any cash advance fees/interest (avoid using credit cards at ATMs)

- Pick your trio:

- Primary spending card: no-FX-fee credit card if you have one.

- ATM card: debit card with low or refunded international ATM fees.

- Backup card: another credit or debit card stored separately.

- Order some local cash. Enough for day one or two, from your bank or a reputable online service – not the airport.

- Decide on a travel card (optional). If you’ll be in one region for a while, a multi-currency card can be worth it.

- Set up mobile wallet. Add your best travel card to Apple Pay/Google Pay for extra security and convenience.

On the trip, I stick to these rules:

- Pay with credit card in local currency whenever possible to avoid extra exchange rate markup on cards.

- Use debit card at bank ATMs for cash, in larger, less frequent withdrawals.

- Keep only a day’s worth of cash in my wallet; the rest stays locked away.

- Store backup cards in a different bag or hotel safe.

- Say

no

to DCC every single time.

When you add it all up, the best payment method for travel costs isn’t one magic card or app. It’s a deliberate mix of cash, debit, credit and mobile wallets, used in the right situations, with the fee traps turned off.

Set it up once, and every future trip gets cheaper – without you having to think about it much at all.