I used to think I was good with money on the road. I hunted for cheap flights, booked apartments with kitchens, and tracked every coffee in a spreadsheet. Then I went through my bank statements after a long trip.

The flights weren’t the problem. The hotels weren’t the problem. The problem was the invisible stuff: exchange rate markups, foreign ATM fees, and a little trap on payment screens called Dynamic Currency Conversion (DCC).

This guide is about those quiet leaks that wreck a carefully planned international travel budget—and how to plug them before your next trip.

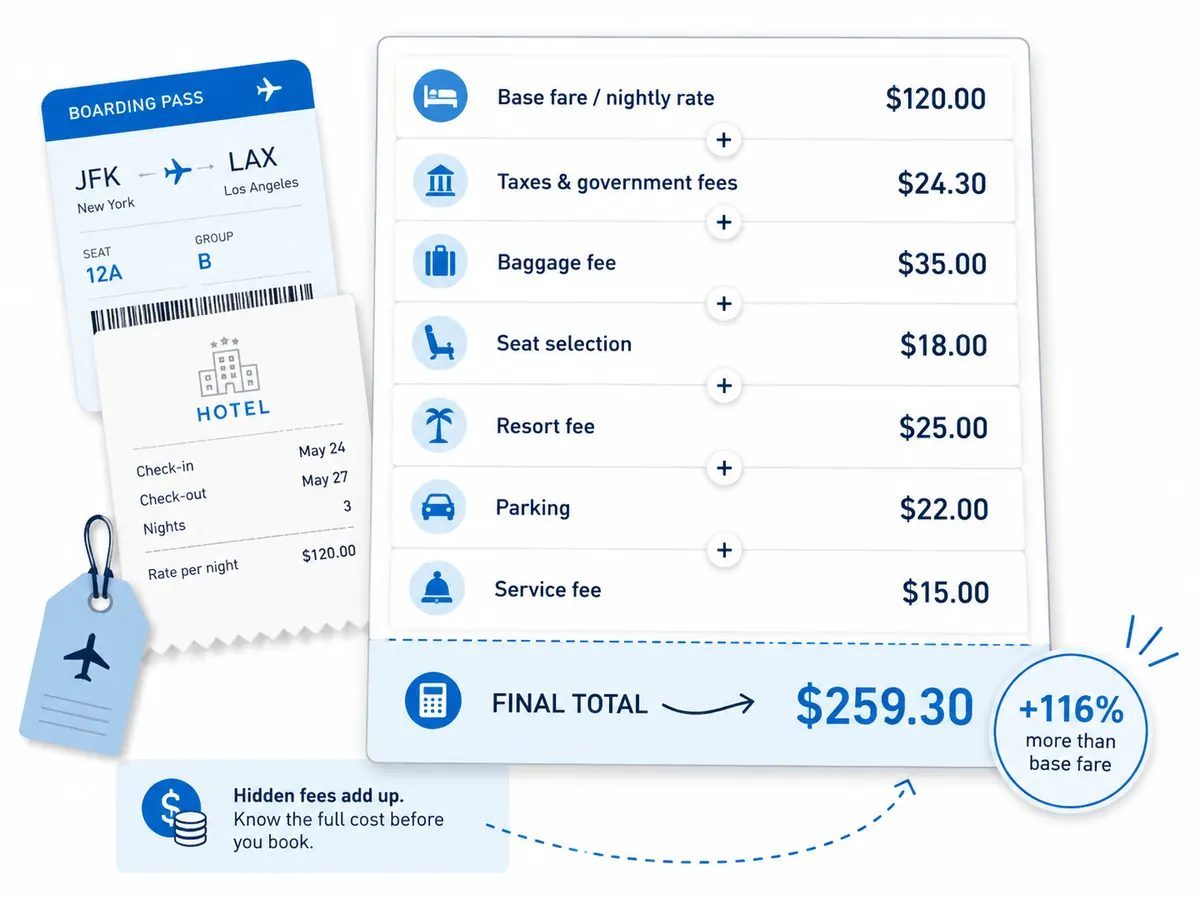

1. The Hidden Stack: How a Simple ATM Withdrawal Becomes a 5–10% Tax

Let’s start with the most common money drain: getting cash abroad.

On the surface, it looks simple. You put your card in a foreign ATM, take out the equivalent of $200, and your bank converts it. Done, right?

Not quite. In reality, up to four different players can take a cut of that one withdrawal, quietly adding to your foreign ATM fees and travel budget:

- Your home bank’s ATM fee – often a flat $2–$5 per withdrawal.

- Your home bank’s foreign transaction fee – usually 1–3% of the amount.

- The foreign ATM operator’s surcharge – another $2–$10+ per withdrawal, especially in tourist zones (source).

- Exchange rate markup – a hidden spread baked into the rate you get, often a few percent.

Put that together and a “$200” withdrawal can easily cost you $215 or more once everything settles. Do that five or six times on a trip and you’ve just tipped an extra $75–$100 to banks and ATM operators for nothing.

Here’s the uncomfortable part: you almost never see the full cost on the screen.

The ATM might show you its own fee. Your bank might show you a “preview” rate in the app. But the real conversion happens later at settlement, at a different rate, with spreads and hidden currency conversion fees layered in (source).

Takeaway: Every withdrawal is a stack of small charges. Your job is to reduce how many stacks you trigger—and how fat each layer is.

2. Bank vs. ATM: Who’s Actually Ripping You Off?

When a withdrawal feels expensive, it’s easy to blame the nearest machine. But the real cost is usually a tug-of-war between your bank and the local ATM operator.

Here’s how the roles split when you’re dealing with overseas card charges and hidden costs:

- Your bank or card issuer controls:

- Foreign transaction fee (1–3% is common).

- Flat out-of-network ATM fee ($2–$5 per withdrawal).

- Any extra markup they add on top of the card network’s FX rate.

- The foreign ATM operator controls:

- The local ATM surcharge (often $2–$10+).

- Whether they push DCC and how aggressively.

Some banks are simply hostile to travelers. Many big U.S. names routinely charge around $5 per foreign ATM withdrawal plus a percentage fee (source). That’s before the foreign ATM adds its own surcharge.

On the other hand, some accounts are built for travel. They:

- Reimburse global ATM fees (including foreign operator surcharges).

- Charge no foreign transaction fee.

- Use near-interbank FX rates with minimal spread.

Then there are the ATMs themselves. A few patterns show up again and again:

- Independent ATMs in tourist areas (airports, convenience stores, near attractions) tend to be the worst offenders, with high surcharges and aggressive DCC prompts.

- Bank-branded ATMs attached to real branches usually have lower or no local fees, especially in many European countries (source).

Takeaway: If you feel ripped off, it’s rarely just one villain. Your bank and the local ATM are both taking their slice. You can choose better versions of both and avoid a lot of hidden bank fees on international trips.

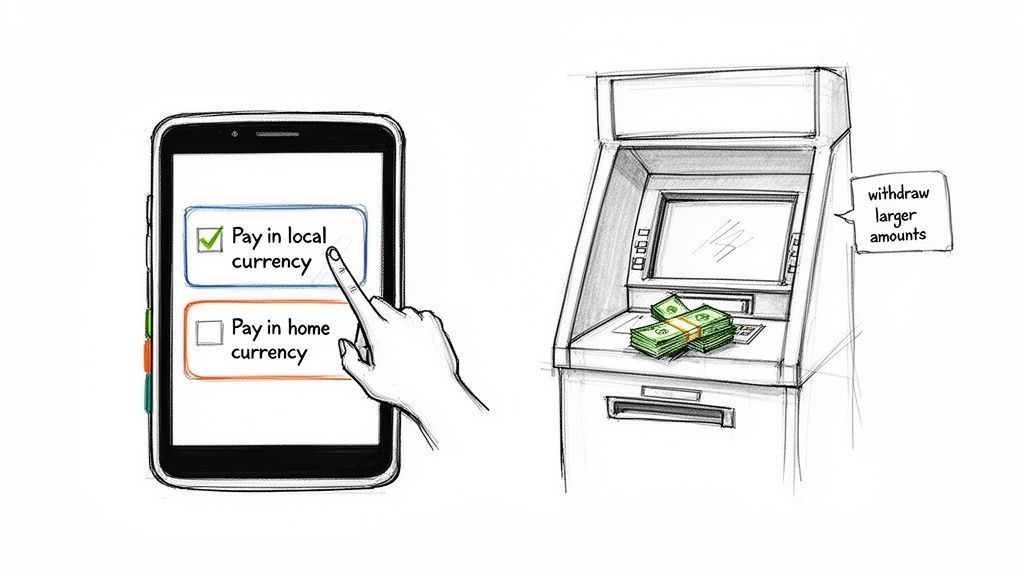

3. The Dynamic Currency Conversion Trap: The Button That Costs You 5–7% Instantly

If there’s one on-the-spot decision that quietly destroys travel budgets, it’s this:

Do you want to pay in your home currency or the local currency?

This is Dynamic Currency Conversion (DCC). It shows up at ATMs and card terminals. It’s marketed as a convenience: See the price in your own currency!

But here’s what’s really happening in this dynamic currency conversion travel trap:

- The merchant’s bank or the ATM’s processor sets the exchange rate.

- They bake in a hefty markup – often 3–7%, sometimes more (source).

- You lock in that bad rate on the spot.

Worse, if your card also charges a foreign transaction fee, you can end up paying twice: once via the terrible DCC rate, and again via your bank’s fee (source).

On a small coffee, that’s annoying. On a hotel bill or a car rental deposit, it’s brutal. You can easily add tens of dollars to a single transaction for no benefit at all.

The prompts are often designed to trick you:

- They highlight the home currency option in green or as “recommended”.

- They use confusing wording like

accept conversion

vs.continue without conversion

. - They may show scary warnings if you choose local currency.

Ignore the drama. The simple rule that saves you money over and over:

Always choose to pay in the local currency.

Whenever you’re asked whether to pay in local currency or home currency abroad, pick local. Let your own bank or travel card handle the conversion. Their rate is almost always better than the DCC rate, even if your bank isn’t perfect (source).

Takeaway: When a terminal or ATM offers to charge you in your home currency, treat it as a paid “feature” you don’t need. Say no. Choose local currency every time. In the battle of dynamic currency conversion vs local currency, local wins almost every time.

4. Airport Kiosks, Tourist ATMs, and Other “Conveniences” That Bleed You Dry

When you land in a new country, tired and slightly disoriented, the money traps are waiting right where you are: at the airport.

Two of the worst offenders:

- Airport currency exchange counters

- Independent ATMs in high-traffic tourist spots

Airport exchange desks often offer rates that are 8–15% worse than the interbank rate, plus commissions on top (source). They’re not scams; they’re just very expensive.

Tourist-zone ATMs and exchange booths play a similar game:

- They advertise

no commission

but hide the cost in a terrible rate. - They add high fixed surcharges per withdrawal.

- Some booths have been caught short-changing or passing counterfeit bills (source).

Meanwhile, a bank ATM in the city center might give you a much fairer deal with no local surcharge at all.

So what do you do when you land and need cash for a taxi or train?

- Use airport options only for a small, immediate amount – enough to get into town.

- Once you’re away from the airport, find a major bank’s ATM attached to a branch.

- Avoid freestanding, flashy ATMs in convenience stores and tourist strips; they’re often the most expensive (source).

Takeaway: Convenience at the airport and in tourist zones is priced aggressively. Use it sparingly, then switch to bank ATMs and better tools as soon as you can.

5. How Many Cards Do You Really Need? Building a Simple, Low-Fee Setup

You don’t need a wallet full of fintech cards to travel smart. But relying on your everyday domestic debit card is usually a mistake if you care about managing exchange rate risk for vacations.

A clean, practical setup looks like this:

- A no-foreign-transaction-fee credit card for purchases

- Use it for hotels, restaurants, tickets, and online bookings.

- Make sure it charges 0% foreign transaction fee – this is where a good credit card foreign transaction fee comparison pays off.

- Never use it for ATM withdrawals – that’s usually treated as a cash advance with immediate interest and extra fees (source).

- A travel-friendly debit card for cash withdrawals

- Look for accounts that:

- Rebate or waive global ATM fees.

- Charge no foreign transaction fee.

- Use fair FX rates with minimal spread (source).

- Some “free ATM” cards have monthly limits – after a certain amount, they start charging percentage fees on withdrawals (source). Know your limit.

- A backup card from a different provider

- Cards get lost, swallowed by ATMs, or blocked.

- Having a second card (ideally from a different bank or network) is cheap insurance.

Then set simple rules for yourself:

- Card for spending, debit for cash.

- Local currency only at terminals and ATMs.

- Fewer, larger withdrawals instead of many small ones, as long as it’s safe to carry the cash.

Takeaway: Two good cards (plus a backup) beat one bad all-purpose card. Separate tools for purchases and cash, and you’ll cut a big chunk of hidden costs.

6. Planning Your Cash Strategy: How Often Should You Actually Hit the ATM?

Once you understand how fees stack, the next question is obvious: How often should I withdraw?

There’s a trade-off:

- Many small withdrawals = more flat fees (your bank’s ATM fee + local surcharge each time).

- Fewer large withdrawals = fewer fees, but more cash to carry and manage.

Because so many fees are per transaction, it’s usually cheaper to withdraw larger amounts less often. For example:

- Five withdrawals of $40 with a $5 total fee each time = $25 in fees.

- One withdrawal of $200 with a $5 total fee = $5 in fees.

Same total cash, very different cost.

But there are two catches:

- Some travel cards have monthly fee-free limits. Go over, and they start charging a percentage on each withdrawal (source).

- Carrying too much cash is a security risk. You need a number that feels safe for you.

A practical approach:

- Estimate how much cash you actually need per day (many places are card-friendly now).

- Plan to withdraw enough for 3–5 days at a time, not every day.

- Store most of it in a secure place (hotel safe, money belt, hidden wallet), and carry only what you need.

Takeaway: Your goal isn’t to avoid ATMs completely. It’s to use them deliberately, in the right places, at the right frequency.

7. How to Tell If You’re Being Overcharged (Without Becoming Obsessed)

You don’t need to turn every purchase into a math exercise. But a few quick checks can tell you if you’re getting a fair deal or being quietly drained by exchange rate shocks and travel costs.

Here’s a simple way to sanity-check costs and estimate your travel money fees:

- Know the real rate

- Before and during your trip, check the mid-market rate with a reliable converter (Google, XE, Wise, etc.).

- This is your baseline – what banks trade at, not what you’ll actually get.

- Compare big transactions

- For larger payments (hotel bills, tours, car rentals), do a quick mental or app check.

- If the rate you’re effectively getting is 5–10% worse than the mid-market rate, something’s off – usually DCC or a bad exchange counter (source).

- Audit one day of spending

- Pick a day, note what you spent in local currency, and later compare it to what hit your statement.

- Look for patterns: repeated DCC, high ATM surcharges, or a card that’s consistently giving you a bad rate.

Once you see the pattern, you can adjust: switch cards, change where you withdraw, or refuse DCC more aggressively. Over time, this is how you quietly avoid hidden currency conversion fees when traveling.

Takeaway: You don’t need perfect precision. You just need to notice when the gap between the real rate and what you’re getting is too big to ignore.

8. The Mindset Shift: From “I’ll Deal With It Later” to “I Decide How My Money Moves”

Most travelers lose money on exchange rates and ATM fees not because they’re careless, but because the system is designed to be opaque. The costs are scattered:

- A few dollars here in ATM surcharges.

- A few percent there in FX spreads.

- A sneaky DCC markup on a hotel bill.

Individually, they feel small. Together, over a multi-day trip, they can add up to hundreds of dollars in pure friction (source).

The shift is simple, but powerful:

- You stop letting random machines and merchants decide how your money is converted.

- You choose which card does the conversion, where you withdraw, and when you accept fees.

In practice, that means:

- Setting up at least one travel-friendly card before you go.

- Using airport and tourist-zone options only as a last resort.

- Always paying in local currency and refusing DCC.

- Withdrawing cash strategically instead of impulsively.

If you do just those things, you’ll already be ahead of most travelers. And the money you don’t hand to banks and ATMs? That’s another night out, another day trip, another reason your future self will be glad you paid attention to the real cost of moving money across borders.

In the end, it’s not about never paying fees. It’s about deciding which ones are worth it—and keeping the rest in your pocket.