I love the idea of flexible

travel. I hate what it does to most people’s budgets.

On paper, flexible flights sound perfect: pay a bit more now, relax later if plans change. In reality, that bit more

can be huge, and the flexibility is often less generous than the marketing suggests.

In this guide, I’ll walk you through how flexible tickets really work, where the hidden costs live, and how to stay genuinely agile without burning cash. Think of this as a practical, slightly skeptical playbook for people who want options and value.

1. The First Trap: Thinking “Flexible” Means “Free to Change Anything”

Let’s start with the biggest misconception: assuming a flexible ticket is a magic pass.

Most flexible or flex

fares do not mean unlimited, penalty-free changes. They usually mean:

- Lower or no change fee from the airline, but…

- You still pay any fare difference between your old and new flight.

- Many cancellations give you credit, not cash back.

So if your original ticket was $400 and the new date is now $750, your no change fee

flexibility still costs you $350. The airline just waived a $100–$200 penalty. Helpful, yes. Free, no.

Here’s the mindset shift that saves money: flexible = cheaper to change, not free to change.

Before you pay extra for flexible airfare, it’s worth doing a 60-second reality check:

- Open the airline’s fare rules (usually a small link near the price).

- Look specifically for: change fee, refund type (cash vs credit), expiry date, and same-day change rules.

- Ignore the marketing name (Flex, Saver, Value, Semi-Flex). Names are branding; rules are reality.

If the rules are vague, full of exceptions, or buried in legalese, that’s your first red flag. That’s where the hidden costs of flexible flights usually hide.

2. The Real Math: When Paying More Upfront Actually Makes Sense

Buying a flexible ticket is basically buying built-in insurance. You pay more now so the airline takes on some of the risk that your plans change.

So the real question isn’t Is flexibility good?

It’s:

Is the extra cost lower than the realistic risk of needing to change or cancel?

Here’s a simple way to think about flexible vs non-refundable airfare cost.

Step 1: Compare prices

- Non-refundable fare: $300

- Semi-flexible fare: $380

- Difference (your

insurance premium

): $80

Step 2: Estimate your risk

Ask yourself honestly: What are the chances I’ll need to change or cancel?

- Low (under 20%) – plans are solid, dates fixed, no big uncertainties.

- Medium (20–40%) – some moving parts: work, visas, family, health.

- High (40%+) – you already suspect something might shift.

Step 3: Estimate the damage if things go wrong

- If you cancel a non-refundable ticket, how much do you lose? (Often most of it.)

- If you rebook last-minute, how much more might the new ticket cost?

Once the chance of change hits roughly 30–40%, the expected cost of losing the fare plus paying higher last-minute prices often beats the extra you’d pay for a flexible ticket. That’s when flexibility starts to look smart.

On the other hand, if you’re booking a $90 short-haul flight and the flexible version is $160, paying $70 extra to protect a $90 ticket is usually a bad bet unless a change is almost guaranteed.

In other words: cheap ticket = you can afford to gamble more. For many trips, a non-refundable fare plus a good backup plan is a better budget strategy for flexible travel than paying for the most flexible ticket on the page.

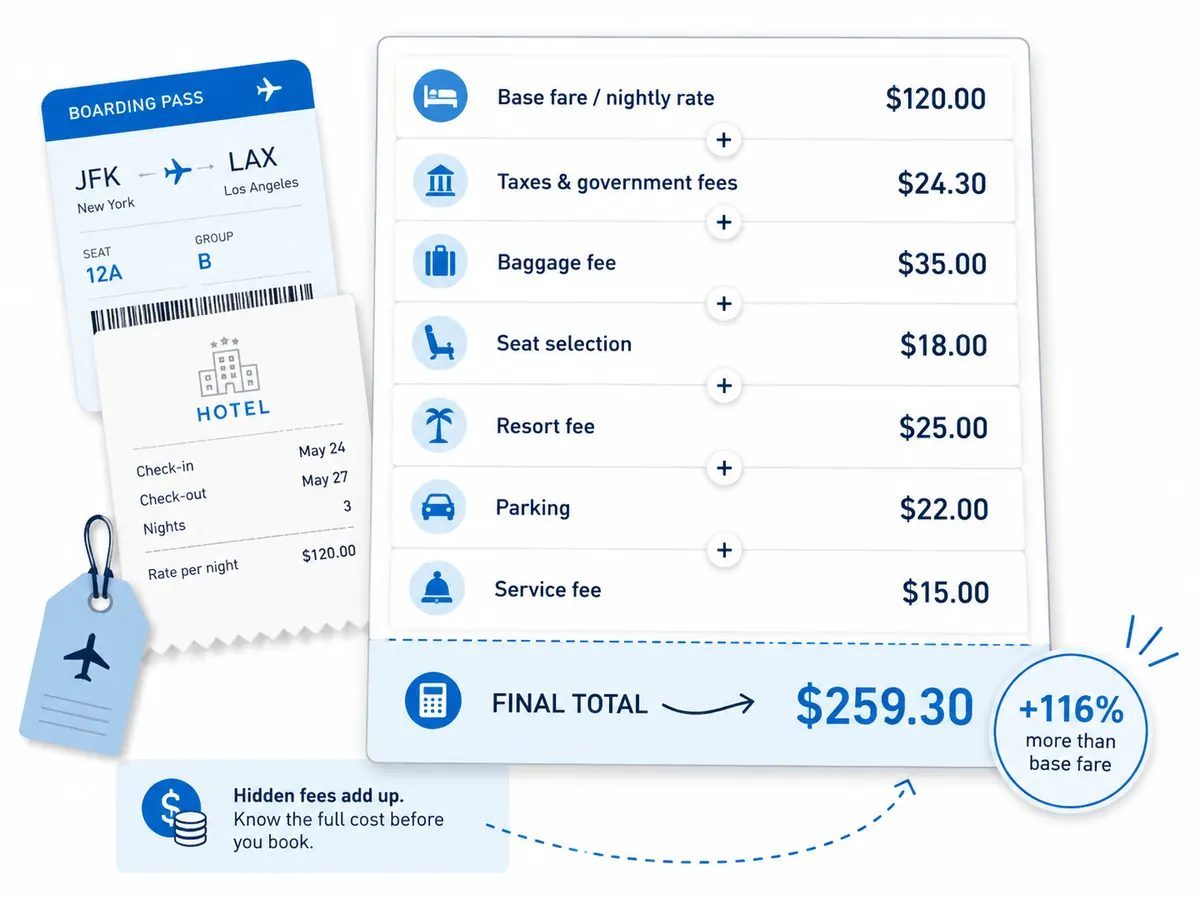

3. Change Fees vs Fare Differences: The Hidden Budget Killer

Airlines love to advertise No change fees!

It sounds generous. It’s also only half the story.

There are two separate costs when you change a flight:

- Change fee – the fixed penalty (often $0–$200) the airline charges.

- Fare difference – the gap between what you paid and what the new flight costs now.

Flexible tickets usually remove or reduce the fee, but they almost never protect you from fare differences. That’s where people get burned, especially if they don’t understand how airline change fees and fare differences work together.

Example:

- Original ticket: $450

- New date (same route, same cabin): $800

- Change fee: $0 (because you bought a flexible fare)

- Fare difference: $350 – you still pay this.

So yes, you avoided a $150 fee. But you still paid $350 more. The real cost of changing was $350, not $0.

Here’s how I handle this in practice:

- For peak seasons (Christmas, summer, big events): I often book earlier and consider a semi-flexible fare. Prices tend to rise, so locking in a lower base fare with some flexibility can be worth it.

- For off-peak or routine trips: I’m more comfortable with non-refundable tickets and just accept the risk.

- For business travel: I pay close attention to same-day change rules and whether my company will cover fare differences or only fees.

The key is to stop thinking no change fee = safe

and start thinking: What will this change actually cost me if prices jump?

That’s the real flexible ticket cost breakdown that matters.

4. Credits, Refunds and Expiry Dates: The Fine Print That Bites Later

Another hidden cost of flexible

travel: what you get back when you cancel is often not cash.

Most flexible or changeable fares work like this:

- You cancel your flight.

- The airline issues a travel credit or voucher.

- The credit has an expiry date (often 12–24 months).

- It may be usable only by the original passenger, sometimes only on certain routes.

If you don’t rebook in time, that flexibility

quietly turns into lost money.

Here’s what I do to avoid that:

- Track credits – I keep a simple note or spreadsheet with airline, amount, expiry date, and booking reference.

- Set reminders – I put calendar alerts 2–3 months before each credit expires.

- Check who can use it – some airlines allow name changes or family use, others don’t.

Also, don’t confuse refundable with flexible:

- Flexible/changeable – you can change or cancel with low/no fee, but usually get credit.

- Refundable – you can cancel and get money back to your card.

Refundable fares are often much more expensive, but for big, once-a-year trips where losing the money would really hurt, they can be worth considering. If you’re wondering are flexible tickets worth it?

, this is where your own risk tolerance matters more than the airline’s marketing.

5. When Flexible Tickets Are Actually Worth the Money

So when does paying extra for flexibility make sense? I look at three things: trip value, uncertainty, and pain level.

Flexible tickets are usually worth it when:

- Your plans depend on something outside your control

Pending visas, embassy appointments, job offers, medical results, or family situations. If a delay or denial would force you to move dates, flexibility is a safety net. - The trip is expensive or rare

Long-haul flights, big annual vacations, or trips where last-minute rebooking would be financially painful. - Your schedule is volatile

Business travel with shifting meetings, kids’ school calendars in flux, or work that often changes at short notice. - You’re traveling in peak season

When you know prices will spike closer to departure, locking in a flexible fare early can be cheaper than rebooking from scratch later.

Flexible tickets are usually not worth it when:

- Your dates are truly fixed (weddings, exams, non-movable events).

- The flight is cheap and losing the fare wouldn’t hurt much.

- You already have other protection (good travel insurance, employer flexibility, or credit card coverage).

One more nuance: some flexible fares include extras like baggage, seat selection, or priority boarding. If you’d pay for those anyway, the flexibility premium

is effectively lower than it looks. Always compare what’s bundled when you’re doing your own flexible airfare pricing guide in your head.

6. Non-Refundable vs Flexible: A Simple Risk Checklist

When I’m staring at two fares – one cheap and rigid, one pricier and flexible – I run through a quick checklist. You can steal it.

Question 1: How likely is a change?

- Under 20% – I lean non-refundable.

- 20–40% – I compare the flexibility premium vs potential loss carefully.

- Over 40% – I lean flexible or refundable.

Question 2: How painful would losing this money be?

- Annoying but manageable – I might gamble on non-refundable.

- Financially stressful – I treat flexibility as insurance.

Question 3: What’s the realistic worst-case scenario?

- Lose $150 on a short flight? Maybe acceptable.

- Lose $1,200 on a long-haul family ticket? That’s a different story.

Question 4: Do I already have backup?

- Does my credit card offer trip interruption or cancellation coverage?

- Will my employer cover change fees or fare differences for work trips?

- Do I have travel insurance that covers the specific risks I’m worried about (illness, family emergencies, etc.)?

Non-refundable tickets aren’t bad

. They’re just a bet. The key is to make that bet consciously, not because the cheaper price seduced you in the moment. Understanding fare difference charges and basic airline fare rules and flexibility will keep you from making the most common mistakes with flexible flight tickets.

7. Budget Tactics to Stay Agile Without Overpaying

If you like flexibility but hate overpaying (same), here are some tactics I actually use.

1. Mix and match flexibility

- Make the most uncertain leg flexible (often the outbound).

- Keep the more predictable leg non-refundable.

- On family trips, sometimes only the person with the unstable schedule gets a flexible ticket.

This is one of the cheapest ways to stay flexible when flying without buying fully flexible fares for everyone.

2. Use semi-flexible fares strategically

Fully flexible/refundable tickets can be overkill. Semi-flexible fares (low change fee, credit on cancellation) often hit a sweet spot between cost and protection. They’re a solid budget strategy for flexible travel when you know there’s some risk, but not chaos.

3. Book early for peaks, later for off-peak

- For Christmas, summer, or major events: book earlier, consider some flexibility.

- For shoulder seasons or low-demand routes: you can often wait longer and keep things non-refundable.

4. Treat travel insurance as a tool, not a magic wand

Sometimes a solid insurance policy is cheaper than paying for flexible fares on every leg. But read the conditions: insurance doesn’t make non-refundable tickets magically refundable for any reason. It covers specific events. If you want to know how to avoid airline change fees entirely, the honest answer is: you usually can’t, but you can shift some risk to insurance instead of the airline.

5. Watch same-day change rules

On some airlines, same-day confirmed changes are cheap or even free (especially with elite status). If your risk is mostly same day

timing shifts rather than full date changes, this can save you from paying for a more expensive flexible fare.

6. Don’t hoard credits

If you have airline credits, plan trips around them before they expire. A forgotten $300 credit is the most expensive kind of flexibility. Treat those credits like cash with a timer on them.

8. A Simple Way to Decide, Every Time

Whenever you’re about to click Continue

on a flight booking, pause for 30 seconds and ask yourself:

1. What exactly does this fare let me do if plans change?

If you can’t answer that, you haven’t read the rules enough.

2. How likely is a change, really?

Not the optimistic version. The honest one.

3. Am I okay with losing this money or paying more later?

If the answer is absolutely not

, flexibility (or even refundable) is worth a closer look.

Flexible travel isn’t about buying the most expensive, most generous ticket every time. It’s about using flexibility as a targeted tool – paying for it when the risk is real, and skipping it when it’s just fear or marketing pressure.

If you start treating every ticket as a small risk decision instead of a simple price comparison, you’ll stay agile and keep more money for the part of travel that actually matters: the trip itself.