I love the ease of tapping a card overseas. No fumbling for coins, no mental math. But after years of trips (and a few ugly bank statements), I’ve realised something uncomfortable: your card can quietly burn 5–10% of your travel budget in foreign transaction fees and bad exchange rates. Sometimes, going a bit more old-school with cash isn’t just cheaper – it actually feels safer and more in control.

In this guide, I’ll walk you through the money traps I now avoid, when I deliberately choose cash over card, and how to build a simple travel money plan that doesn’t rely on blind trust in your bank.

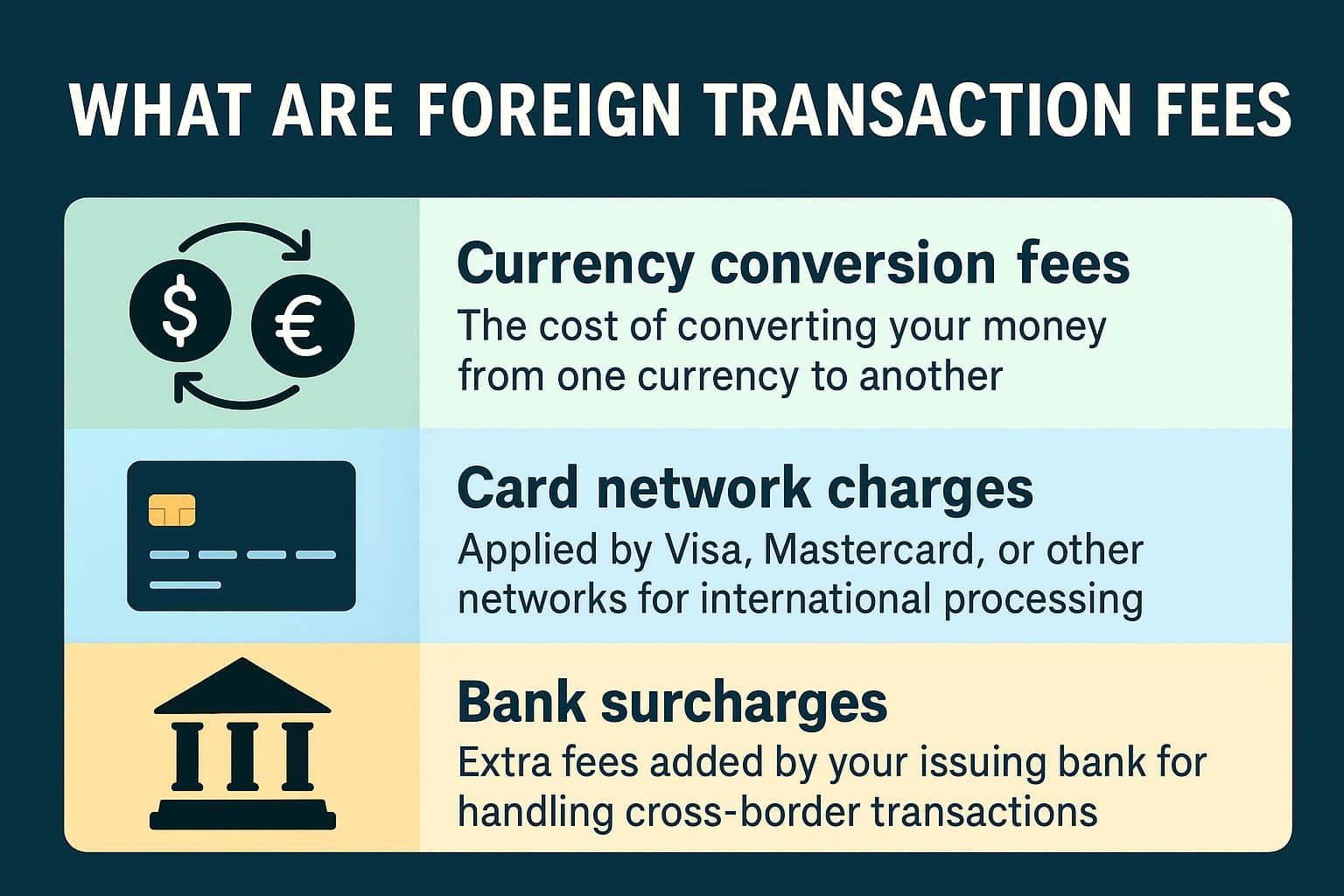

1. The Invisible Tax on Every Tap: FX Margins & Foreign Transaction Fees

Every time you pay by card abroad, there are usually two layers of cost:

- Foreign transaction fee – often 1–3% of every purchase.

- Hidden FX margin – the bank’s mark-up on the exchange rate, sometimes another 2–4% on top of the real mid-market rate.

Put together, that “free” tap can quietly cost you 3–7% extra on every transaction. On a $2,000 trip, that’s $60–$140 gone for nothing – no extra service, no extra comfort, just friction in the system.

The problem is that these costs are rarely obvious:

- The exchange rate looks “official”, but it’s padded compared to the live rate.

- Fees are often baked into the transaction instead of clearly itemized.

- Vague labels like

international service assessment

orcross-border fee

hide what’s really going on.

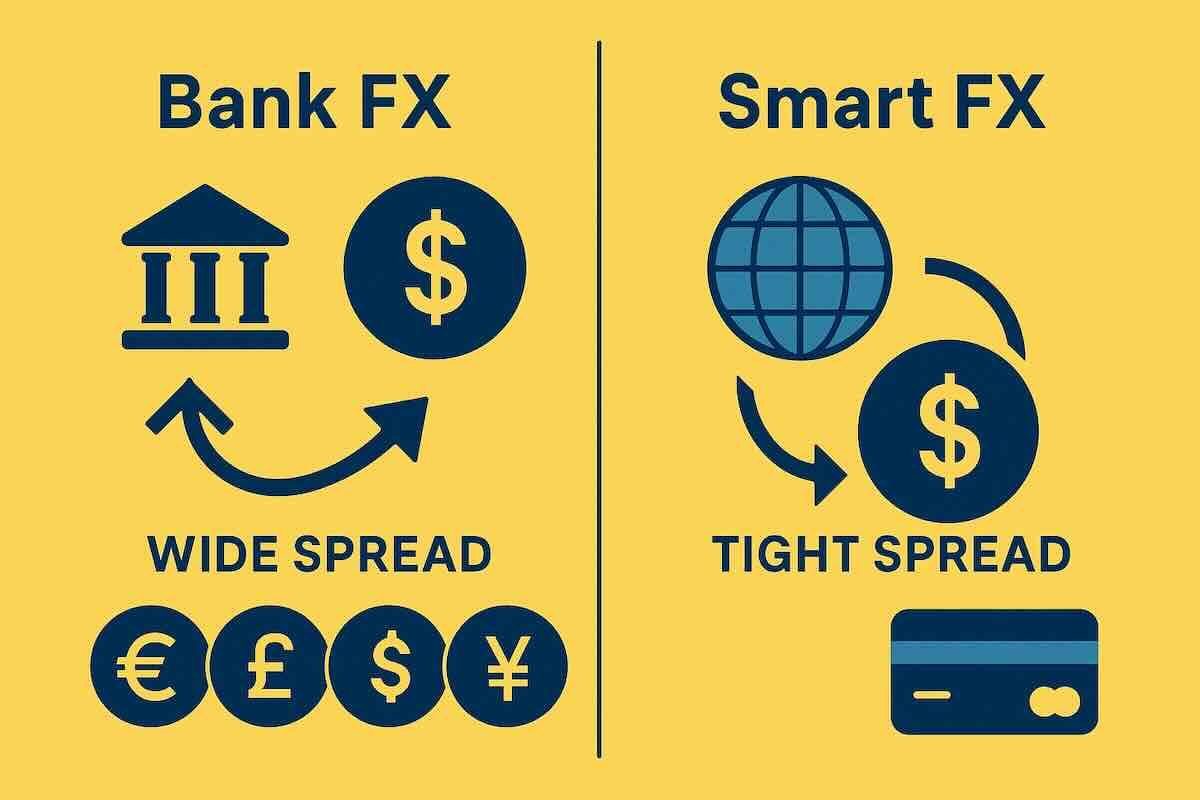

Once I started comparing my card’s rate to the mid-market rate (on sites like XE or Wise), I realised how much I was leaking on foreign transaction fees while traveling. That’s when I began asking before every trip: Is this card actually worth using abroad, or is there a cheaper way to pay?

Takeaway: If your card adds foreign transaction fees and uses a padded exchange rate, then cash (from a decent ATM or pre-ordered currency) can instantly be cheaper for everyday spending than paying by card abroad.

2. The Dynamic Currency Conversion Trap: The One Button You Must Always Refuse

If you remember only one thing from this guide, make it this:

When a terminal or ATM abroad asks, “Pay in your home currency or local currency?” always choose local currency.

This little choice is called Dynamic Currency Conversion (DCC). It sounds helpful: the machine “kindly” converts the price into your home currency so you know exactly what you’re paying. In reality, it’s a money-maker for the merchant or ATM operator and one of the biggest hidden costs of paying by card abroad.

Here’s what usually happens with DCC:

- The terminal uses a terrible exchange rate, often 4–8% worse than your card network (Visa/Mastercard).

- There may be extra “service” or “conversion” fees on top.

- You lose the benefit of your card network’s relatively fair rate.

I’ve seen ATMs in touristy parts of Europe and Asia offering DCC rates that were 7–10% worse than the real rate. That’s like tipping the machine for no reason at all.

So my rule is simple:

- At shops and restaurants: “Charge me in local currency, please.”

- At ATMs: if it offers to convert to your home currency, decline and continue in local currency.

Takeaway: Dynamic currency conversion charges are almost never in your favour. Paying in local currency and letting your bank or card network handle the conversion is nearly always the cheapest way to pay abroad.

3. ATMs vs Airport Kiosks: The Lesser Evil (and When Cash Wins)

Everyone knows airport exchange kiosks are bad. What most people underestimate is how bad.

Airport kiosks typically hit you with:

- Very wide buy/sell spreads – in other words, ugly exchange rates.

- Upfront commissions or “service fees”.

- “No fee” offers where the cost is simply hidden in a worse rate.

Compared to that, bank ATMs in your destination are usually the lesser evil. Even with a flat ATM fee, the underlying rate is often much closer to the real market rate, especially if you avoid DCC.

But ATMs have their own traps when you’re comparing card vs cash abroad fees:

- Your home bank may charge an international or out-of-network fee.

- The local ATM operator may add a surcharge.

- Both are often flat per withdrawal, so lots of small withdrawals get expensive fast.

Here’s how I make cash cheaper than using a high-fee card overseas:

- Use real bank ATMs, not random “tourist” machines in bars, souvenir shops, or next to ticket booths.

- Withdraw larger amounts less often (within what you’re comfortable carrying) so the flat fee is spread over more cash.

- Always decline DCC at the ATM and choose local currency.

- Check if your bank has global ATM partners that waive or refund foreign ATM fees.

In many countries, this approach makes cash from ATMs cheaper than paying by a high-fee card for small, everyday purchases like coffee, buses, and snacks.

Takeaway: If your card has steep overseas charges, using a low-fee ATM to pull out a sensible chunk of cash can beat tapping your card for every little purchase.

4. When Cash Is Actually Safer (Yes, Really)

We’re often told that cards are always safer than cash. That’s only half the story.

Cards are safer if:

- You’re making big bookings (flights, hotels, car rentals).

- You want chargeback protection or built-in insurance.

- You’re in a place where pickpocketing is common and you’d rather lose plastic than a wad of notes.

But cash can be safer in a different way when you think about international card payment mistakes and fraud risks:

- It can’t be skimmed at a dodgy terminal.

- It can’t be cloned and used online for months after your trip.

- It doesn’t expose your main bank account every time you pay.

I’ve had my card details skimmed at a perfectly normal-looking restaurant in Europe. The fraud was caught, but my main card was frozen mid-trip. Not fun. Since then, I’ve changed how I think about the “safe way to carry money when traveling”.

- I keep a modest amount of local cash for day-to-day spending.

- I use a separate travel card (often a multi-currency card) with limited funds for taps and online payments.

- I store backup cards and extra cash separately – hotel safe, a different bag, or a money belt.

Cash also protects you from a different headache: “card not accepted”. Outside big cities, you’ll still run into:

- Cash-only taxis and buses.

- Street food stalls, markets, and family-run shops that don’t take cards.

- Guides and small tour operators who prefer cash (and sometimes offer a better price for it).

Takeaway: A small, well-managed stash of cash plus a limited-funds travel card can be safer and more flexible than relying on one main card for everything.

5. The Psychology of Spending: Why Cash Helps You Stay on Budget

There’s a cost to cards that never shows up as a line item: you usually spend more when it doesn’t feel like real money.

When I travel with only cards, I notice the pattern:

- Another coffee? Tap.

- Another round of drinks? Tap.

- Random souvenir I’ll forget about in a week? Tap.

It’s frictionless. And that’s exactly why it’s dangerous for your budget.

With cash, every purchase is a tiny reality check. You see the notes leaving your wallet. You feel the exchange rate. It’s much easier to pause and think, Is this really worth it?

Here’s how I use cash as a simple budgeting tool when weighing currency exchange vs card fees:

- At the start of each day, I take out a fixed amount of cash for food, transport, and small treats.

- When it’s gone, I’m done with casual spending for the day (unless there’s a genuine need).

- Big, planned expenses (museum passes, special dinners, activities) go on a card I’ve chosen for low fees and decent rewards.

This split keeps my daily spending under control and helps avoid that “how did I spend that much?” moment when I get home and see the statement.

Takeaway: Cash makes spending visible and tangible. If you tend to overspend with contactless payments, using cash for daily expenses can save you more than any clever fee hack.

6. Multi-Currency Travel Cards: The Middle Ground Between Cash and Credit

If you don’t want to carry too much cash but you’re wary of your regular bank card, multi-currency travel cards (like Wise or Revolut) are a great middle ground between cash and credit.

Why I like them for keeping credit card fees overseas under control:

- You can hold multiple currencies and convert at or near the mid-market rate.

- Fees are usually transparent and lower than traditional banks.

- You can top up as you go, keeping only limited funds on the card.

- They often include virtual cards for safer online bookings.

My typical setup now looks like this:

- Before the trip, I move some money into a travel money card and convert a portion into the destination currency when rates look reasonable.

- I use that card for most card payments (always choosing to pay in local currency, never my home currency).

- I withdraw cash from ATMs using the same card, staying within its free or low-fee limits.

- I keep a no-foreign-transaction-fee credit card as backup for big purchases and emergencies.

This way, I dodge a lot of hidden costs of paying by card abroad, avoid nasty debit card charges abroad, and still don’t have to carry a thick roll of notes.

Takeaway: A good multi-currency travel card plus a modest cash buffer often beats using your regular bank card abroad – both in cost and in peace of mind.

7. A Simple, Low-Stress Money Plan for Your Next Trip

Let’s turn all this into something you can actually use. Here’s the simple travel cost guide I follow now for paying by card abroad without getting stung.

Before you go

- Check your existing cards: foreign transaction fees, ATM fees, and any global ATM partners that refund charges.

- Get at least one no-foreign-transaction-fee option (credit or travel card) if you can.

- Order a small amount of foreign cash from a reputable provider if you’ll arrive late, or in a cash-heavy destination.

- Set up alerts on your accounts so you spot suspicious charges quickly.

On arrival

- Avoid airport exchange kiosks unless you’re desperate.

- Use a bank ATM to withdraw a sensible amount of cash (not tiny amounts every day).

- Split your money: some cash in your wallet, some in your bag or hotel safe, plus a backup card stored separately.

During the trip

- Use cash for small, everyday expenses and places that clearly prefer it.

- Use your best-value card (no FX fee, fair rate) for big purchases and online bookings.

- Always pay in local currency and decline DCC at terminals and ATMs.

- Check your accounts every few days for odd or duplicate charges.

If you follow this, you’ll usually:

- Pay less in hidden card fees, bad exchange rates, and dynamic currency conversion charges.

- Be less vulnerable to card fraud, skimming, or losing access to your main account.

- Stay more aware of your spending and avoid budget shock when you get home.

Final thought: You don’t have to choose between “all card” or “all cash”. The sweet spot is a smart mix: cheap cash for the small stuff, a good travel card for most payments, and your regular credit card as backup. Once you see how much you save on foreign transaction fees and card vs cash abroad fees, it’s hard to go back to tapping blindly.