I don’t buy travel insurance because I’m scared. I buy it because I’ve done the math.

When I talk to other travelers, I hear the same two lines over and over:

I’ll just self-insure with a big emergency fund.

I always buy the most expensive policy so I’m fully covered.

Both can backfire.

Your real safety net abroad is a mix of cash you control and risks you hand off to an insurer. The smart move isn’t choosing one or the other. It’s deciding which risks you’ll cover with your own money and which you’ll outsource.

That balance changes by country, by trip style, and by your own finances. So let’s walk through how to split your safety net like a numbers-first traveler would.

1. What Should Insurance Do vs What Your Emergency Fund Should Do?

Before you compare policies or calculate how much travel emergency fund you need, draw a clear line between the two tools:

- Insurance is for low-probability, high-cost disasters you can’t comfortably pay for.

- Emergency fund is for high-probability, low-to-medium cost hassles you can absorb without wrecking your life.

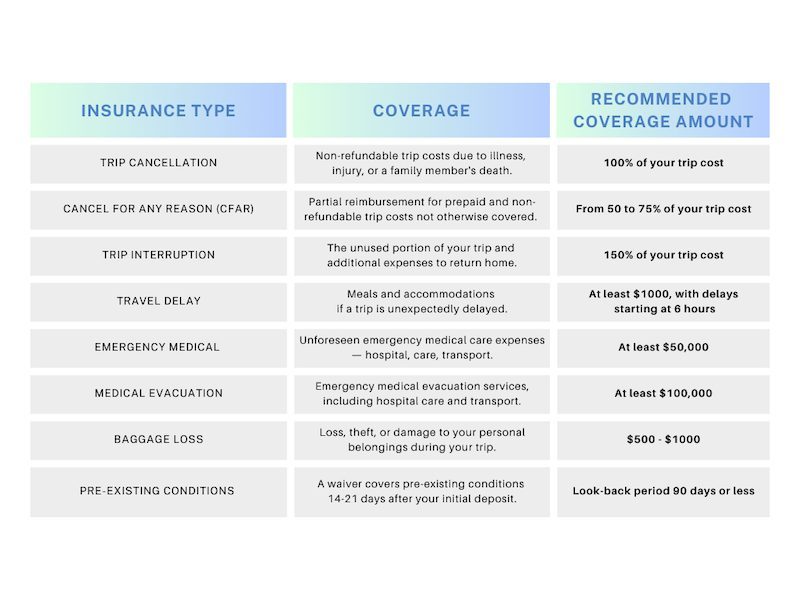

Most travel insurance is really a bundle of different protections (see Squaremouth and the CDC Yellow Book):

- Trip cancellation / interruption – protects prepaid, non-refundable costs.

- Emergency medical – covers illness or injury abroad.

- Medical evacuation – gets you to a hospital that can actually treat you.

- Delay / missed connection – hotels, meals, catching up to your trip.

- Baggage delay / loss – clothes, essentials, replacement items.

Now layer your emergency fund on top of that:

- If losing the money would sting but not cripple you, that’s a good job for your emergency fund.

- If losing the money would seriously damage your finances, that’s a strong candidate for insurance.

So the real question isn’t Should I buy travel insurance?

It’s this: Which specific risks am I willing to self-insure with my own cash, and which ones do I want to transfer to an insurer?

Once you see it as self-insuring vs buying travel insurance for each type of risk, the decisions get much clearer.

2. How Your Destination Changes the Insurance vs Cash Split

Most insurers don’t price your policy by destination in a detailed way, but you absolutely should choose coverage based on destination risk (as Allianz notes in their guide).

Think of it as a simple travel safety net strategy: the more expensive or complicated the medical system, the more you lean on insurance for health and evacuation, and let your emergency fund handle the rest.

High-cost medical countries (US, Canada, Japan, Singapore, some Caribbean islands)

- Hospital stays and ER visits can run into tens of thousands of dollars.

- Even a simple broken bone can turn into a four-figure bill.

My split here:

- Insurance: High emergency medical limits + strong medical evacuation.

- Emergency fund: Small stuff – taxis, extra hotel nights, minor delays.

In these countries, trying to cover travel medical costs without insurance is a big bet. I’d rather pay a modest premium than risk a five-figure hospital bill.

Moderate-cost, good public healthcare (most of Western Europe, UK, Australia, New Zealand)

- Costs are lower than the US, but still painful for non-residents.

- Care quality is high, but you may need private care or pay upfront.

My split here:

- Insurance: Solid medical + evacuation, but limits don’t need to be extreme.

- Emergency fund: More room to self-insure trip delays and some baggage issues.

For many travelers, this is where the balance between travel insurance vs emergency fund starts to feel flexible. You still want protection, but you don’t need sky-high limits.

Lower-cost but higher-risk or remote (parts of Southeast Asia, Latin America, Africa, Central Asia)

- Basic care can be cheap, but serious issues may require evacuation to another city or country.

- Remote areas can make transport extremely expensive.

My split here:

- Insurance: Very strong medical evacuation, decent medical coverage.

- Emergency fund: Local clinic visits, minor injuries, small travel hiccups.

Here, the real financial risk isn’t the clinic bill. It’s the helicopter, the air ambulance, or the international transfer.

Cruises and expedition-style trips

- Shipboard medical care is not cheap and often out-of-network.

- Evacuation from a ship or remote region can be brutally expensive.

My split here:

- Insurance: Top-tier medical + evacuation, plus trip interruption (missing the ship is costly).

- Emergency fund: On-the-ground expenses once you’re off the ship.

Notice the pattern: as medical systems get more expensive or logistically complex, I lean harder on insurance for health and evacuation, and let my emergency fund handle the everyday annoyances.

3. How Big Should Your Emergency Fund Be While Traveling?

Let’s talk cash. Not vague I’ll figure it out

money, but actual numbers you can move or withdraw.

When I plan a trip, I ask myself one question:

- How much could I realistically need to spend in 48 hours if everything went sideways?

That usually includes:

- 1–3 nights of last-minute accommodation.

- Rebooking a flight or buying a new one-way ticket.

- Basic food and local transport.

- Some medical costs before insurance kicks in or reimburses.

For many travelers, that works out to roughly:

- $500–$1,000 for budget trips in cheaper regions.

- $1,000–$2,000+ for trips involving expensive cities, cruises, or peak-season flights.

That’s your travel emergency fund – the part of your safety net you’re willing to put at risk on the road.

But remember, your emergency fund isn’t just for travel. It’s also your buffer if you come home to a job loss, a broken car, or a rent hike. So I split it mentally:

- Core emergency fund (at home): 3–6 months of living expenses.

- Travel buffer: The extra amount I’m willing to risk on this trip.

Then I match that to insurance:

- If my travel buffer is small, I buy more insurance (higher medical, better trip interruption).

- If my travel buffer is large, I can safely self-insure more (lower trip cancellation, maybe skip baggage coverage).

Allianz frames it as: How much can you afford to lose?

I’d tweak that to: How much can you afford to lose without derailing your long-term goals?

4. Trip Cost, Non-Refundables, and When Cancellation Coverage Is Worth It

Trip cancellation is where a lot of people either overpay or leave themselves exposed.

According to Squaremouth, cancellation coverage is meant to protect prepaid, non-refundable costs. Not the emotional value of your trip. Just the money you can’t get back.

Before I buy a policy, I do a quick exercise:

- List every major cost: flights, hotels, tours, cruises, trains.

- Mark each as refundable, partially refundable, or non-refundable.

- Add up only the non-refundable portion.

That total is what I insure for trip cancellation/interruption. Not more.

Then I ask:

- If I lost this entire non-refundable amount tomorrow, would it hurt or would it be catastrophic?

A few examples:

- $800 weekend trip you could easily replace: I might skip cancellation coverage and rely on my emergency fund.

- $8,000 family safari with strict cancellation rules: I’d insure the full non-refundable amount.

- Long-term travel with mostly flexible bookings: I might insure only key flights and big deposits.

One more wrinkle in your travel risk management budget: annual vs single-trip plans. As Allianz points out, annual plans often have a cap on total cancellation benefits for the whole year. If you stack multiple expensive trips, you can hit that cap quickly.

In that case, I sometimes:

- Use an annual plan for medical/evacuation.

- Buy separate single-trip cancellation coverage for the one big, non-refundable trip.

5. Medical & Medevac: The One Area I Rarely Self-Insure

This is the part of the travel insurance vs emergency fund debate where I’m least willing to gamble.

The CDC is blunt: your domestic health insurance may not cover you abroad, or may cover only a fraction of costs, and many foreign hospitals want payment upfront (source).

So I separate two questions:

- What does my existing health insurance cover abroad?

- What would a serious emergency cost in the countries I’m visiting?

Then I decide how much of that risk I want to offload.

My personal rules of thumb for international travel medical coverage cost and limits:

- Emergency medical: I aim for at least $100,000 coverage for most international trips, more if I’m going somewhere with very high medical costs or doing riskier activities.

- Medical evacuation: I like to see $250,000–$500,000+, especially for cruises, remote areas, or countries with limited advanced care.

Why so high? Because medevac is where the numbers get ugly. Helicopters, air ambulances, and cross-border transfers add up fast.

Could I self-insure this with my emergency fund? Maybe, if I had a seven-figure portfolio and was comfortable risking a big chunk of it. Most people aren’t. I’m not.

So this is where I’m happy to pay a relatively small premium to avoid a potentially life-altering bill.

One more layer: pre-existing conditions. If you have them, you need a plan that explicitly covers them and you have to follow the rules (timing of purchase, stability periods, etc.), as Allianz notes. This is not an area to guess or assume.

6. Long Trips, Digital Nomads, and When Annual or Long-Term Plans Make Sense

If you’re gone for months, the balance between emergency savings vs insurance for travelers shifts again.

Long-term travel insurance (3–24 months) is built for exactly this, as explained in Capture the Atlas. These plans usually focus on:

- Emergency medical.

- Evacuation and repatriation.

- Some baggage and delay coverage.

But they’re not a full replacement for local health insurance if you’re actually moving abroad. They’re designed for extended travel, not permanent relocation.

Here’s how I decide between options for long-term travel and digital nomad emergency fund planning:

- Multiple short trips (e.g., 4–6 trips/year, each under 45–90 days)

→ I look at an annual multi-trip plan for medical/evacuation and maybe light cancellation coverage. - One long trip (e.g., 6–12 months continuous)

→ I look at a long-term single-trip policy with strong medical/evacuation and accept that I’ll self-insure more of the small stuff.

For long trips, I also adjust my emergency fund strategy:

- I keep a larger buffer accessible at home (not all in local cash).

- I assume I’ll have more minor issues (delays, lost items) and plan to self-insure many of them.

- I still rely on insurance for the big medical and evacuation risks.

The longer you’re on the road, the more likely something will go wrong. Insurance handles the catastrophic tail risk; your emergency fund handles the inevitable friction.

7. Cash Emergencies, Theft, and What Insurance Really Does (and Doesn’t) Cover

There’s a persistent myth that insurance will bail me out if I lose my money.

Not really.

As PolicyBazaar explains, emergency cash benefits are tightly controlled:

- They usually apply only to theft, robbery, or baggage loss, not simple misplacement.

- You often need a police report or airline Property Irregularity Report.

- You must prove you actually had the money (bank statements, ATM slips, etc.).

- There are strict time limits to report the incident.

Even then, the insurer may just help coordinate funds from your family or send a limited amount, minus fees. It’s a lifeline, not a blank check.

So for money access, my Plan A looks like this:

- Multiple cards, kept in different places.

- A small amount of local cash + backup currency (like USD or EUR in some regions).

- Online banking and someone at home who can help if needed.

Insurance is the backup, not the main strategy.

Same with baggage. I assume I’ll replace essentials out of pocket first, then treat any insurance reimbursement as a bonus. That mindset keeps me from over-insuring my stuff and under-insuring my health.

8. A Simple Framework to Decide Your Split for Any Trip

Let’s turn all of this into a simple travel safety net strategy you can reuse for any trip, whether you’re planning a quick getaway or long-term travel.

Step 1 – Map your non-refundable costs

- Calculate the total non-refundable portion of your trip.

- Ask:

If I lost this tomorrow, would it be painful or catastrophic?

- If catastrophic → insure it. If just painful → consider self-insuring with your emergency fund.

Step 2 – Assess destination medical and evacuation risk

- High-cost or remote destination? Lean toward higher medical + evacuation limits.

- Good, affordable healthcare? You can be more moderate, but I’d still want solid coverage.

Step 3 – Check your existing coverage

- Call your health insurer:

What’s covered abroad? Emergency only? Any evacuation?

- Check your credit cards: what travel protections do they actually offer, and under what conditions?

- Treat these as supplements, not replacements, unless you’ve read the fine print carefully.

Step 4 – Decide your travel emergency fund size

- Estimate 2–3 days of worst-case expenses (last-minute flights, hotels, food).

- Add a buffer for minor medical costs and delays.

- Make sure this doesn’t compromise your core at-home emergency fund.

Step 5 – Choose the right type of plan

- Single-trip plan for big, one-off vacations or long journeys.

- Annual multi-trip plan if you travel frequently and want consistent medical/evacuation coverage.

- Long-term travel plan if you’re gone 3–24 months without returning home.

Step 6 – Decide what you’re consciously self-insuring

- Write down:

I am choosing to self-insure X, Y, Z with my emergency fund.

- That might be: small delays, some baggage loss, cheap domestic flights, or low-cost weekend trips.

- If writing it down makes you nervous, that’s a sign you might want coverage there.

In the end, the goal isn’t to be fearless or paranoid. It’s to be deliberate.

Use insurance for the stuff that could wreck you. Use your emergency fund for the stuff that will just annoy you. And adjust both knobs—coverage and cash—based on where you’re going, how long you’re gone, and how much risk you’re honestly willing to carry.